This blog is also available on Substack. Follow along there for addition insights into the artisanal spirits sector and supply chain technology.

The $500 Billion Laboratory

On August 7, 2025, when 15% tariffs hit European wine imports, something unexpected happened. Instead of market collapse, we witnessed the most dramatic reshuffling of global trade patterns in decades—and it's only the beginning.

French wine exports to the US surged 23% in value and 37% in volume during H1 2025. Spanish producers captured fourth-largest supplier status by pivoting to the $10-$20 retail segment. Italian wines maintained volume leadership despite tariff headwinds.

This isn't just about wine. The $500 billion global wine industry has become an inadvertent laboratory for understanding how the new tariff-heavy trade regime will reshape every category of artisanal trade—from craft spirits to specialty foods to luxury goods.

The producers who understand these patterns first will capture disproportionate value. Those who don't will find themselves margin-squeezed into irrelevance.

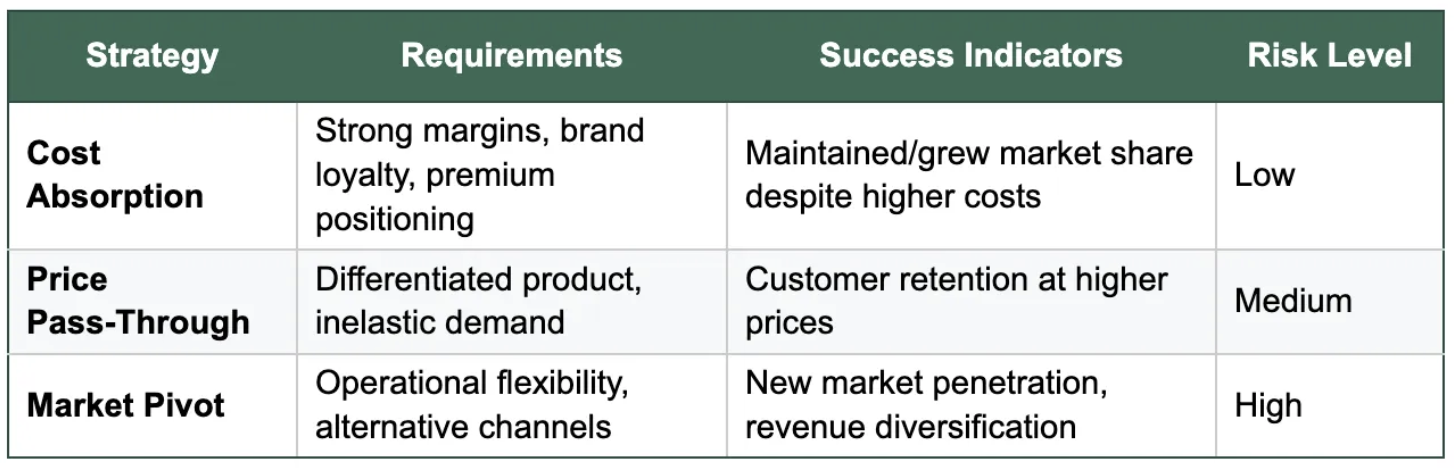

The Tariff Absorption Framework

Think of tariffs like a sudden increase in your rent. You have three options: absorb the cost, pass it through to customers, or find a cheaper location. The wine data reveals which strategy works—and why.

The Absorption Winners:

- France: Absorbed 15% tariff cost, gained 23% value growth

- Italy: Maintained volume leadership at 128.2 million liters

- Spain: Strategic pivot to $10-$20 segment, achieved supplier status upgrade

The Pass-Through Strugglers:

- Mass market wines: Unable to pass through costs without losing customers

- Mid-tier brands: Caught between premium positioning and price sensitivity

- Generic imports: Commoditized products with no pricing power

The Framework:

Strategic Insight: Premium authentic brands can absorb tariff shocks because they have pricing power and customer loyalty. Mass producers get margin-squeezed because they compete on price alone.

For artisanal spirits producers, this model is directly applicable. Mexican agave spirits enjoy USMCA tariff-free access, but 40% have documentation deficiencies. The opportunity belongs to producers who get compliance right while building premium positioning that can weather future trade volatility.

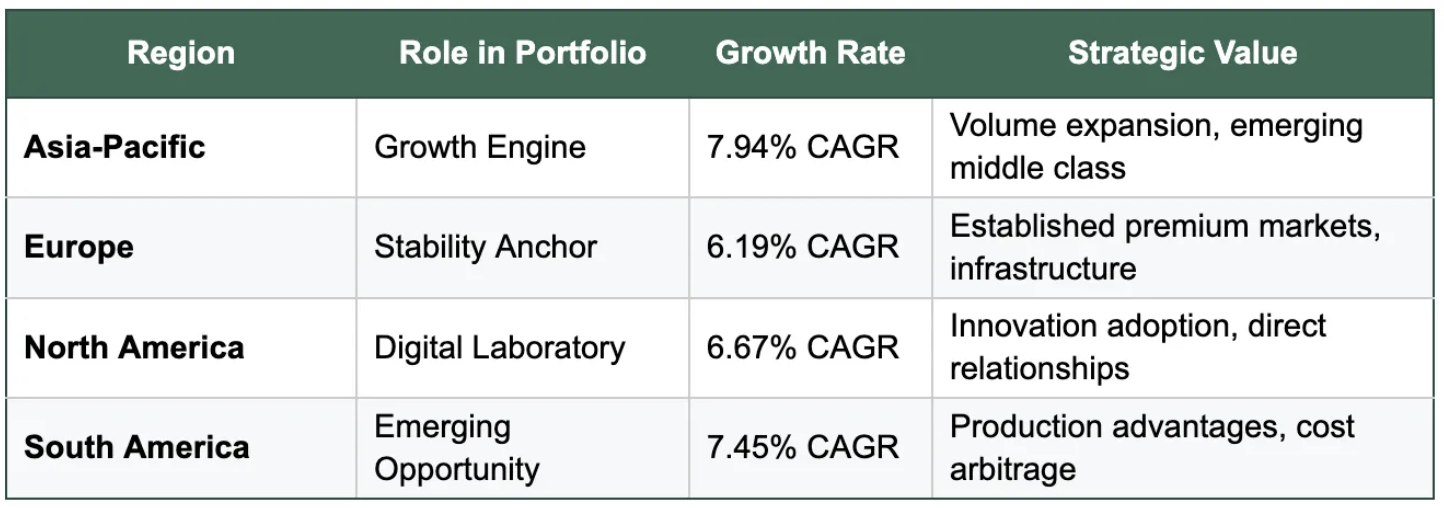

The Geographic Arbitrage Engine

The new trade regime creates geographic arbitrage opportunities that didn't exist under the old globalization model. Smart producers are building what I call "trade route portfolios" instead of single-market strategies.

Asia-Pacific: The Growth Engine

- India: 6% beverage alcohol growth, 19% premium-plus expansion

- Southeast Asia: 2% consistent growth across Philippines, Thailand, Vietnam

- China: Market stabilizing (-4% vs. -8% previous year)

Europe: The Stability Anchor

- 37.71% global market share ($187.98 billion)

- Sophisticated distribution infrastructure

- Premium positioning acceptance

North America: The Digital Laboratory

- 39.4% of global online wine sales

- Direct-to-consumer adoption

- Premium price point acceptance

The Geographic Diversification Model:

Rule of Thirds Application: No single market should exceed 33% of revenue. European wine producers demonstrate that geographic diversity provides resilience against trade tensions. When tariffs hit one region, growth in others compensates.

The strategic opportunity for artisanal producers is building portfolios that balance growth (Asia-Pacific), stability (Europe), and innovation (North America) while maintaining authentic brand positioning across different cultural contexts.

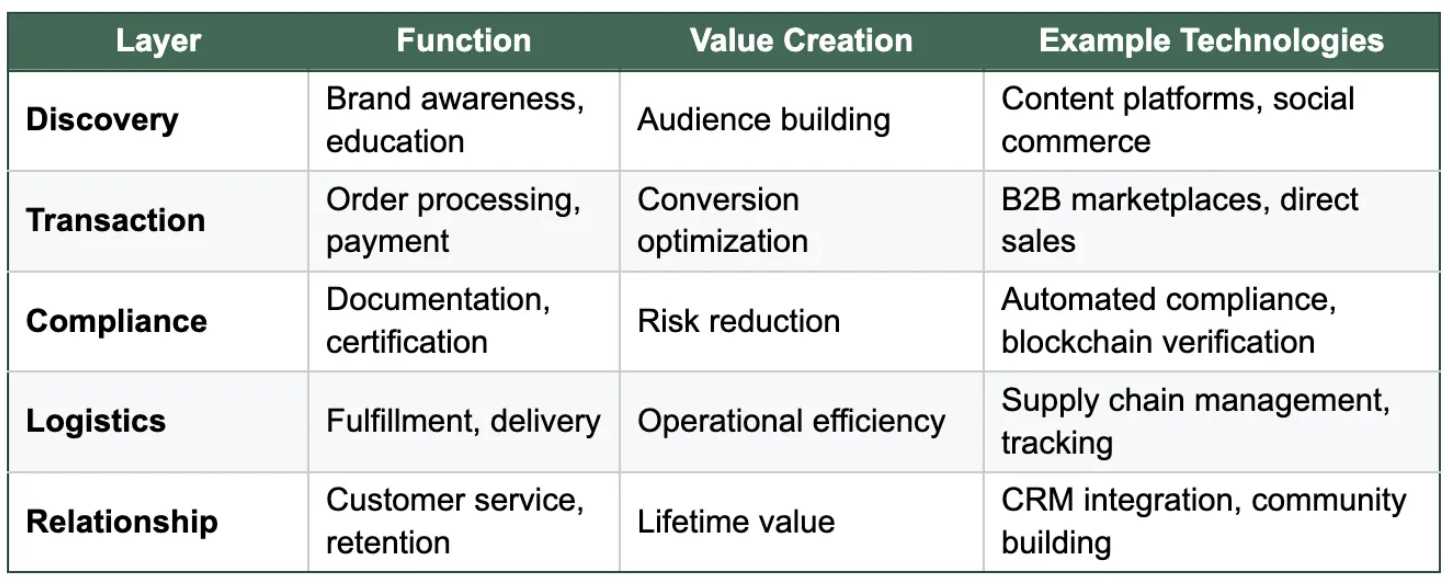

The Digital Distribution Stack

The most profound insight from wine industry data isn't about tariffs—it's about how trade tensions are accelerating the adoption of new distribution infrastructure that bypasses traditional bottlenecks entirely.

Current Distribution Value Capture:

- Traditional Three-Tier: Producers capture 30-40% margin

- Enhanced Traditional: 40-50% margin capture

- Digital Platforms: 60-70% margin capture

- Optimized Multi-Channel: 75-80+ margin capture

The Digital Stack Framework:

Digital Channel Growth Reality:

- Global online wine sales: $23.18 billion (2025) → $40.24 billion (2032)

- Wine subscription market: $12.4 billion → $31.4 billion (2035)

- Asia-Pacific leads with 16.3% global online sales despite lower overall penetration

The winning strategy isn't choosing between traditional and digital distribution—it's building a distribution optimization platform that enhances traditional relationships with digital capabilities while creating new direct channels for growth.

Think Shopify for physical retail. Shopify didn't replace physical stores—it gave them digital capabilities to compete with Amazon. The successful artisanal trade platforms will do the same thing: handle complexity while preserving authentic relationships.

The Contrarian Take: Why Everyone's Wrong About "Premiumization"

Here's where conventional wisdom gets dangerous. Everyone talks about "premiumization" as if it's a universal solution to trade tensions and market pressures. The data tells a different story.

The Premium Paradox:

- Top quartile premium wineries: +22% revenue growth

- Bottom quartile: -16% revenue decline

- But: 73% of "premium" brands are actually getting squeezed in the middle

The dirty secret nobody talks about: Most brands calling themselves "premium" aren't actually premium—they're mass market products with premium pricing that collapses under pressure.

What True Premiumization Requires:

- Authentic Differentiation: Not just higher prices, but genuine scarcity or superior quality

- Cultural Resonance: Connection to place, tradition, or craft that can't be replicated

- Relationship Equity: Direct connections with customers who seek you out specifically

- Operational Excellence: Ability to deliver consistently at scale without losing authenticity

The Middle Market Extinction Event: The $15-$30 price segment—supposedly the "premium sweet spot"—is actually becoming the most dangerous place to compete. You're too expensive for price-sensitive buyers but not differentiated enough for true premium customers.

Contrarian Strategy: Instead of chasing premiumization, focus on authentic positioning that creates genuine pricing power through scarcity, story, or superior experience. Or go completely the other direction: embrace cost leadership and operational efficiency to win on value.

The brands getting crushed are those stuck in the middle, trying to be premium without having premium credentials, or trying to compete on price without cost advantages.

The Brand Strategic Playbook: Positioning for Future Scenarios

The wine industry's response to tariff pressures reveals specific patterns of adaptation that translate directly to strategic positioning for the three emerging paths. Rather than generic advice, here's how successful producers are actually repositioning their operations based on which future they're betting on.

Building Platform Readiness (The Amazon Scenario)

European wine producers succeeding despite tariffs share common characteristics that make them platform-ready:

Data Infrastructure Excellence: The French producers gaining 23% value growth have invested in systems that capture buyer behavior, inventory optimization, and quality metrics. They're not just tracking sales—they're building the data foundation that platforms need to match producers with buyers effectively.

Authentic Storytelling at Scale: Spanish producers pivoting to the $10-$20 segment succeeded because they could communicate authenticity through digital channels without losing credibility. They developed content strategies that educate buyers about terroir, production methods, and cultural heritage—exactly what platform algorithms reward with better discovery.

Operational Transparency: Italian producers maintaining volume leadership despite tariffs implemented end-to-end visibility systems. Buyers on platforms want to see production capacity, quality certifications, and shipping capabilities upfront. The winners made their operations transparent enough to build trust without direct relationships.

Strategic Positioning Actions:

- Develop comprehensive producer profiles that showcase authenticity through data

- Build content libraries that educate rather than just promote

- Implement tracking systems that provide buyer confidence in delivery and quality

- Create operational documentation that enables platform verification

Preparing for Geographic Fragmentation (The Regional Bloc Future)

The Rule of Thirds isn't just risk management—it's preparation for a world where trade relationships determine market access more than product quality.

Regulatory Excellence as Competitive Advantage: The European producers thriving under 15% tariffs invested heavily in compliance before tariffs hit. They understood that regulatory complexity would become a moat protecting them from competitors who couldn't navigate the bureaucracy.

Cultural Embassy Strategy: Successful producers aren't just selling products into new regions—they're becoming cultural ambassadors for their categories. French wine producers in Asia don't just export wine; they export wine education, creating demand for the entire category while positioning themselves as the authentic choice.

Local Partnership Development: Spanish producers' success in achieving fourth-largest US supplier status came through deep local partnerships, not just distribution agreements. They found partners who understood both the Spanish production culture and American market preferences, creating bridges rather than just transactions.

Strategic Positioning Actions:

- Build compliance expertise that exceeds current requirements

- Develop deep cultural knowledge in target markets, not just customer preferences

- Create partnership strategies that share value rather than just access channels

- Invest in local market education that benefits the entire category

Cultivating Authentic Renaissance Positioning (The Craft Heritage Future)

The premium polarization data—top quartile +22%, bottom quartile -16%—reveals that authenticity premiums are already emerging. The question is whether producers can capture them.

Heritage Documentation and Storytelling: The producers commanding premium prices have documented their production methods, family histories, and cultural connections in ways that create genuine scarcity. They're not just making products—they're preserving traditions that buyers can't get anywhere else.

Craft Knowledge as Currency: Premium producers are sharing production knowledge, sustainability practices, and cultural context in ways that educate buyers while demonstrating expertise. They've realized that teaching buyers why their methods matter creates more value than keeping secrets.

Community Building Over Customer Acquisition: The most successful authentic brands aren't chasing customers—they're building communities of people who appreciate craftsmanship. Their marketing feels more like cultural preservation than sales because they're focused on finding the right customers, not more customers.

Strategic Positioning Actions:

- Document production methods and cultural heritage in compelling, shareable formats

- Develop educational content that builds category appreciation, not just brand preference

- Create experiences that connect buyers with production culture and craftsmanship values

- Build communities around shared appreciation for authenticity rather than just products

Three Paths Forward: The Industry's Crossroads

The wine industry's transformation under the new trade regime reveals three distinct paths emerging. Each offers different risk/reward profiles and requires different strategic capabilities.

Path 1: The Platform Consolidation Route

What It Looks Like: Large technology-enabled platforms become the dominant distribution infrastructure, similar to how Amazon transformed retail or Uber transformed transportation.

Winners:

- Platform operators who build network effects and capture transaction value

- Premium producers who maintain brand equity while leveraging platform reach

- Technology providers who enable seamless integration

Losers:

- Traditional distributors who can't adapt to digital-first models

- Mid-tier producers without differentiation or operational efficiency

- Regions/countries with restrictive digital commerce regulations

Preparation Strategy:

- Build direct customer relationships now while developing platform partnerships

- Invest in data capabilities and digital marketing competencies

- Focus on authentic differentiation that can't be commoditized by platform dynamics

Timeline: 3-5 years for platform dominance, 7-10 years for full transformation

Path 2: The Geographic Fragmentation Scenario

What It Looks Like: Trade tensions create permanent regional blocs with distinct supply chains, similar to the Cold War era but organized around trade relationships rather than ideology.

Winners:

- Producers with strong regional positioning and local partnerships

- Countries/regions with favorable trade agreements and cultural ties

- Companies that can operate effectively across multiple regulatory environments

Losers:

- Global brands dependent on seamless international supply chains

- Smaller producers without resources for multi-market compliance

- Regions heavily dependent on exports to hostile trade partners

Preparation Strategy:

- Build deep expertise in 2-3 core markets rather than broad global presence

- Develop compliance and regulatory capabilities as competitive advantages

- Create partnerships with local distributors and cultural ambassadors

Timeline: 5-7 years for bloc stabilization, 10+ years for new equilibrium

Path 3: The Authentic Renaissance Movement

What It Looks Like: Consumer backlash against globalization creates premium demand for locally-produced, culturally-authentic products, similar to the farm-to-table movement in restaurants.

Winners:

- Artisanal producers with genuine cultural authenticity and craft heritage

- Regions with strong terroir and traditional production methods

- Brands that can tell compelling stories about place, tradition, and craftsmanship

Losers:

- Large industrial producers without authentic positioning

- Regions/products dependent on cost advantages rather than quality differentiation

- Brands that prioritized efficiency over authenticity during globalization

Preparation Strategy:

- Invest heavily in authentic storytelling and cultural preservation

- Build direct relationships with consumers who value craftsmanship

- Develop premium positioning that justifies significant price premiums

Timeline: Already beginning, 3-5 years for mainstream adoption

The Smart Money Strategy: Portfolio Approach

The most sophisticated producers won't choose one path—they'll build capabilities across all three while maintaining strategic flexibility.

Immediate Actions (Next 12 Months):

- Audit current positioning across the three scenarios—where are you strongest/weakest?

- Build platform relationships while maintaining direct customer connections

- Develop compliance excellence as a competitive moat in fragmented markets

- Invest in authentic storytelling that creates emotional connection with customers

Medium-term Positioning (1-3 Years):

- Test and learn in emerging markets to understand which path gains momentum

- Build operational flexibility that enables rapid strategy pivots

- Create strategic partnerships across different potential futures

- Develop technology capabilities that enhance rather than replace human relationships

Long-term Optionality (3+ Years):

- Monitor path indicators and allocate resources toward the winning model

- Double down on competitive advantages that remain relevant across scenarios

- Build infrastructure that supports sustainable growth in the new paradigm

The Opportunity Ahead

The wine industry's $500 billion transformation under the new trade regime offers a preview of what's coming across all artisanal trade categories. The patterns are clear, the tools are available, and the early movers are already capturing disproportionate value.

This isn't about choosing between tradition and innovation—it's about using innovation to scale tradition authentically while building the infrastructure that enables global access without cultural compromise.

The next decade belongs to producers who understand that tariffs aren't just costs to be absorbed—they're market signals pointing toward new opportunities for those smart enough to read them.

The Strategic Imperative: Build authentic differentiation that creates pricing power, develop geographic diversification that provides resilience, and invest in technology that enhances rather than replaces the relationships that make artisanal products special.

The transformation has already begun. The question isn't whether it will accelerate—it's whether you'll be positioned to benefit when it does.