This blog is also available on Substack. Follow along there for addition insights into the artisanal spirits sector and supply chain technology.

TL;DR

A distributor’s job is to move boxes from a warehouse to a licensed account. Not to build your brand. Not to develop relationships. Not to create demand. The U.S. spirits industry has spent 70+ years outsourcing both logistics and sales to the same entity, then wondering why most craft brands can’t achieve meaningful velocity.

The data is unambiguous: 90.9% of U.S. craft producers capture only 10.6% of total craft volume, averaging 531 cases per year. The two largest distributors carry thousands of brands — their reps have, at best, minutes of selling attention per brand per week. This is not a distribution failure. It is a sales infrastructure failure. And it was designed into the system from the start.

Every brand that can’t move product blames distribution. The distributor isn’t pushing hard enough. The rep doesn’t call back. The portfolio is too crowded. These diagnoses are understandable. They are also, in almost every case, wrong.

The honest diagnosis: distribution was never designed to be a sales function. It was designed to move product from producers to retailers — compliantly, efficiently, at scale. The industry conflated logistics and sales out of post-Prohibition necessity. That necessity dissolved decades ago. The conflation remained. And the brands that entered distribution without building their own sales infrastructure are paying for it in ways most of them can’t yet name.

The 2025 Craft Spirits Data Project from ACSA and Park Street found that 90.9% of U.S. craft spirits producers capture only 10.6% of total craft volume, averaging 531 cases per year. Former ACSA president Becky Harris counted 45 distillery closures since early 2023; a New York survey found 50% of distillery owners either foresaw closing by end of 2025 or weren’t sure they’d continue. These aren’t brands with bad products. They’re brands that built distribution without building sales.

The Conflation Problem

The three-tier distribution system wasn’t designed as a sales infrastructure. It was designed as a regulatory firewall — a mechanism to prevent the vertical integration and organized crime control that characterized pre-Prohibition markets. Sales got bundled into that structure because distributors needed revenue, so they hired reps. Three generations of brand builders grew up treating “getting distribution” as synonymous with “going to market.”

What a distributor actually does: takes title to goods in bulk, warehouses them, routes trucks to licensed accounts, and deploys reps carrying 80 to 120 SKUs each. What a sales function actually requires: account-specific relationship development, consumer education, demand creation, and brand advocacy. These are different jobs with different incentive structures. One is optimized for logistics efficiency. The other is optimized for brand growth.

The conflation isn’t anyone’s fault. It’s structural. But ignoring it is a choice — and it’s one the data shows most craft brands are still making.

For brands: The question to ask about every distribution relationship isn’t “are they moving cases?” It’s “are they building anything that belongs to us?” Account relationships, consumer education, reorder momentum — these should accrue to the brand. If they accrue only to the distributor, the relationship is logistics, not sales.

The Attention Math Nobody Does Out Loud

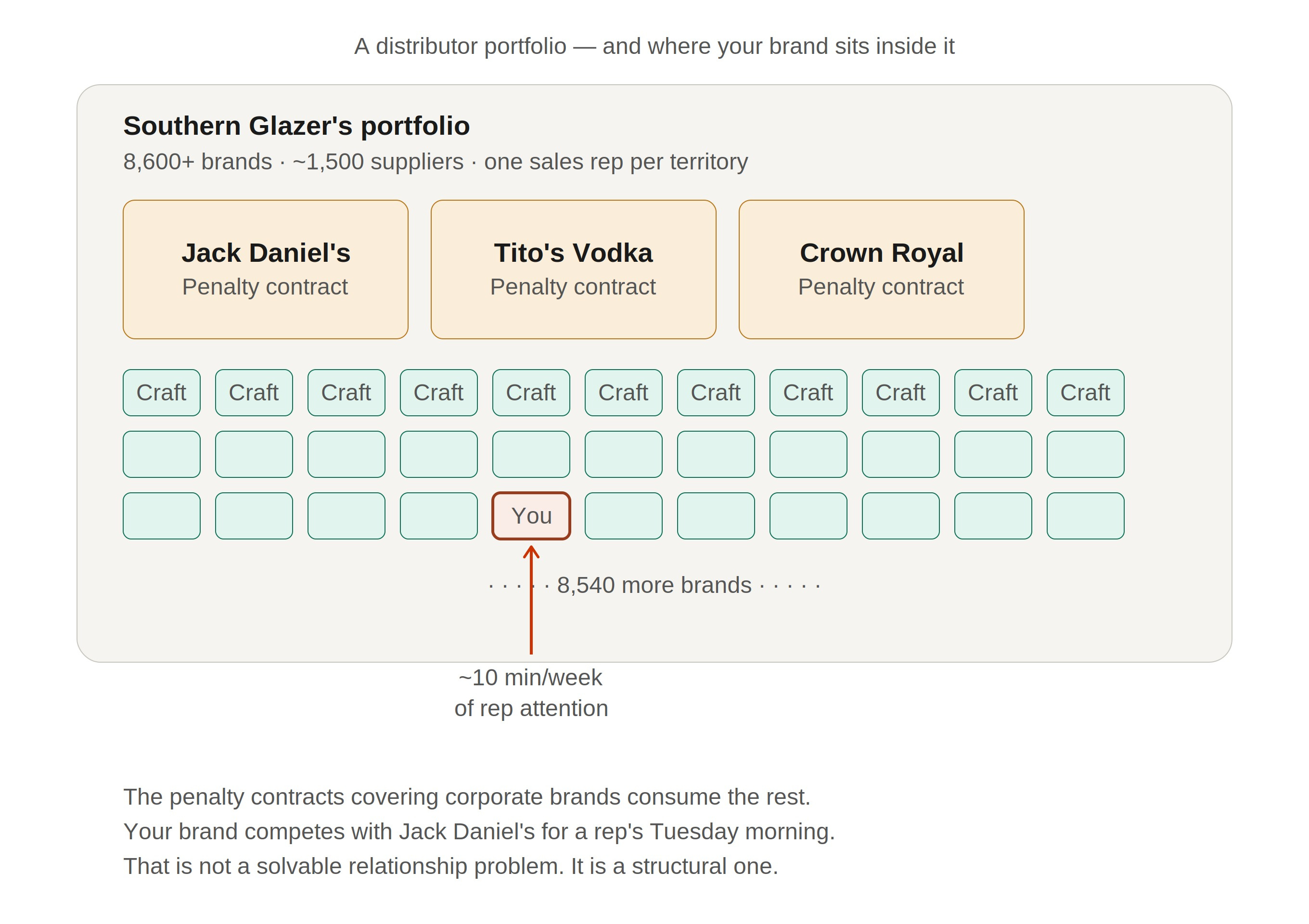

Southern Glazer’s carries over 8,600 brands from approximately 1,500 suppliers across its national portfolio. If a spirits distributor rep carries 300 to 500 active SKUs — consistent with the NBWA’s benchmark showing the average beer distributor now manages 280 brands and 1,100 SKUs across 37 supplier relationships — the allocation math yields approximately 6 to 12 minutes of active selling time per brand per week. Before accounting for order-writing, compliance paperwork, and the mandatory focus on top-tier brands whose contracts include financial penalties for missing volume targets.

Mark Harmon of the Independent Distributor Network put it plainly at Bar Convent Brooklyn in 2024: distributors only have so much time and attention to give, and that allocation follows portfolio optimization logic, not brand development logic. Your craft mezcal isn’t competing with other mezcals in the portfolio. It’s competing with Jack Daniel’s, Tito’s, and Crown Royal for 10 minutes of a rep’s Tuesday.

In February 2026, Breakthru Beverage Group — the third-largest U.S. spirits distributor — laid off approximately 500 employees, cutting a significant portion of field sales personnel. RNDC simultaneously trimmed operations and began divesting state markets to Reyes Beverage Group. The industry’s response to margin pressure is to reduce selling capacity, not increase it. The brands most exposed are the ones that never built any of their own.

For investors: Flat distributor depletion data is not evidence of a demand problem — it may mean the distributor’s rep has never actively pitched the brand to an account. These are different diagnoses with different fixes. The most common single point of failure in craft spirits portfolio companies is treating distribution as a proxy for sales traction.

What ‘In Distribution’ Actually Means

There is a phrase in almost every craft brand pitch deck: “distributed in X states.” It sounds like market traction. In most cases, it is evidence of a contract. Those are different things.

Being “in distribution” means a distributor agreed to carry the brand and purchased initial inventory. It does not mean a rep is actively selling it, that accounts know it exists, or that it is generating meaningful velocity. The ACSA 2025 data makes this gap concrete: small producers do 49.6% of their total business at their own distillery premises and 44.9% in their home state. Out-of-state sales represent just 5.5% of small producer volume. For brands with distribution agreements across multiple states, these numbers raise an uncomfortable question about what those agreements are producing.

Since 2021, home-state share of craft spirits sales has increased 1.1 percentage points while out-of-state share has declined 1.2 points. Producers aren’t expanding their geographic footprint — they’re retreating toward markets where they have direct relationships. That retreat is the industry’s honest verdict on what multi-state distribution produces without owned sales infrastructure supporting it.

Practitioner experience across the industry points to a consistent pattern: nearly half of craft brands fail to secure reorders in a significant percentage of their initial placements. The failure is predictable. A small brand buried in a distributor’s portfolio of thousands generates no pull-through without dedicated field presence. The ACSA’s own conference guidance stated it plainly: “Distributors are fulfillment houses. The selling has to be initiated by your own resources.”

The Invisible Sales Function Transfer

When a brand outsources sales to a distributor, more than market access transfers. Here is what actually moves — and what it costs permanently.

Sources: ACSA/Park Street practitioner guidance; NBWA Distributor Productivity Report (18th ed., 2025); industry consultant interviews.

For operators: Account relationships, sell-through data, and consumer feedback compound over time and create negotiating leverage. When they live in a distributor’s CRM rather than yours, every future distribution conversation starts from zero.

The Consolidation Multiplier

In 1995, the U.S. had approximately 3,000 distributor companies. By 2024, Wine Business Analytics counted 1,054 unique distributors — a 65% reduction during a period when the number of producing brands exploded by an order of magnitude. Each surviving distributor now carries a portfolio far larger than its predecessors. The regional specialist who knew your product and had bandwidth to build it is largely gone.

The disincentive contract era accelerated this. Starting roughly 15 years ago, major suppliers began writing distribution contracts with financial penalty clauses for missing volume targets. Reps who missed Diageo numbers were writing six-figure checks. That concentrated selling energy on brands with the biggest financial consequences for underperformance. Craft brands — carrying no such penalties — moved to the back of every sales bag.

The 2026 RNDC restructuring illustrates where this leads. Reyes Beverage Group — the largest U.S. beer distributor — acquired RNDC operations in 11 states including Texas, Florida, Arizona, Colorado, and Illinois. Their existing priorities are built for volume that most emerging craft brands cannot produce. The brands most vulnerable are the ones whose entire market access strategy runs through the entity being absorbed.

For brands entering new markets: The 65% reduction in the U.S. distributor tier means the distributor who believed in your product and had bandwidth to build it is largely gone. What replaced them optimizes across 8,600+ brands. The business case for owned sales infrastructure has never been stronger — not as philosophy, but as math.

The Pay-to-Play Layer Nobody Budgets For

Even for brands that accept they need to drive their own demand, the economics of doing so through traditional channels are rarely disclosed upfront. The pay-to-play layer is real, largely unwritten, and expensive.

At premium on-premise accounts, honest economics look like this: placement is structured around relationship investment — staff training, cocktail programming, brand activations. At Michelin-starred accounts, this can extend to menu listing fees in the thousands per SKU. The account makes that back in a single weekend. The brand absorbs it as a customer acquisition cost and plans accordingly.

At off-premise retail, slotting fees — where legally permitted — run $250 to $1,000 per SKU per store. A 50-store regional chain placement represents $12,500 to $50,000 upfront before a single bottle sells. Most brands don’t know this before signing distribution agreements that don’t include it.

Texas offers the clearest structural illustration of what happens when the industry is forced to separate logistics from sales. Post-Prohibition law created a literal fourth tier: distributors cannot sell directly to most bars and restaurants. A class of licensed specialists fills that function. The best operators in specific markets — the one who has spent years building relationships at every account inside a major airport complex — are not distributors in the traditional sense. They are sales professionals in a licensed wrapper. Texas forced the separation that the rest of the industry has avoided, and what emerged looks nothing like the bundled model most brands think they’re working with.

For new market entrants: Before signing a distribution agreement for any market, build a complete cost model that includes programming spend: staff education events, on-premise activations, sampling programs, and applicable placement fees. The distributor margin is the cost you know. The programming spend is the cost that typically surprises you. Together, they define whether the market is economically viable at your current volume.

The On-Premise Channel: Contracting, Not Gone

On-premise was where craft spirits built their initial cultural legitimacy. CGA by NIQ research documents that four out of five on-premise guests will change their drink order based on a bartender’s recommendation, and the average bartender influences approximately 11,000 purchase decisions per year. For a brand without marketing budget, the bar was the most efficient trial environment available.

That environment has structurally contracted. Back bars went from an average of 150 spirits SKUs to around 75. Wine lists from 100 to 30. Casual dining has essentially evaporated. TGI Friday’s — once a chain with thousands of U.S. locations — now operates fewer than 100. The 80/20 rule (20% of spirits volume from on-premise) is now closer to 90/10 post-COVID.

On-premise remains the most powerful consumer education mechanism in the category. But the cost of meaningful on-premise presence — in time, programming spend, and selectivity about which accounts are worth pursuing — is now a strategic investment decision, not a baseline assumption. The brand that treats every on-premise account as equally valuable is making the same mistake as the brand that treats every distributor as a functional sales partner.

Craft Spirits Distribution: Where the System Breaks Down

The structural failure points are concentrated and predictable.

Sources: ACSA 2025 Craft Spirits Data Project; NBWA 18th ed. Distributor Productivity Report; Wine Business Analytics; TTB enforcement records; McDermott Will & Emery distribution law guidance; Thoroughbred Spirits Consulting (2025).

For industry observers: The 65% reduction in U.S. distributors and the 90.9% volume concentration in the hands of 1.4% of producers are the same structural problem viewed from different angles. Distribution consolidation created the environment in which only already-scaled brands get attention. That won’t change — which means the brands that survive will be the ones that stopped waiting for it to.

What the System Was Built to Do

The three-tier system does exactly what it was designed to do. It moves product from producers to retailers, compliantly, across all 50 states, through a licensed intermediary tier that prevents vertical integration. As a logistics architecture, it works.

The mistake isn’t the three-tier system. The mistake is treating a logistics architecture as a sales strategy.

The brands that are actually moving product — placing pallets in regional chains, building velocity in specialty off-premise accounts, finding the fourth-tier specialists in markets like Texas who know every account in their territory — aren’t winning because they found a better distributor. They’re winning because someone in their chain is doing actual sales work. The question this article can’t answer for you: is that person on your payroll, or on someone else’s?

Part 2 maps what that sales infrastructure looks like — and the brands that built it before distribution came to them. Part 3 provides the build sequence.

What does your brand’s sales infrastructure actually look like when you strip out the distributor relationship? We’d genuinely like to hear.