This blog is also available on Substack. Follow along there for addition insights into the artisanal spirits sector and supply chain technology.

TL;DR

DTC spirits margins run 65–75% versus 30–35% through traditional distribution—a 6–10x cost advantage when you compare compliance technology ($6K–$33K/year) to the equivalent embedded in distributor margins ($150K+). The compliance technology landscape has matured: Sovos, Avalara, Thirstie, AccelPay, and LibDib/RNDC’s 18-state platform now automate most of what brands thought required a distributor. Wine’s 20-year DTC dataset proves the model works: average winery earns 70% of revenue from DTC; those above 70% DTC outperform on every metric. But 90.9% of craft spirit producers still capture only 10.6% of total volume, and distillery closures are accelerating. This article provides the channel economics, the technology landscape, case evidence from brands that have made the transition, and a phased implementation roadmap.

The companion article mapped the regulatory and legal forces making three-tier more permeable than the industry assumes. This one answers the follow-up question every operator asks: what does it actually cost, what technology exists, who’s done it, and how long does the transition take?

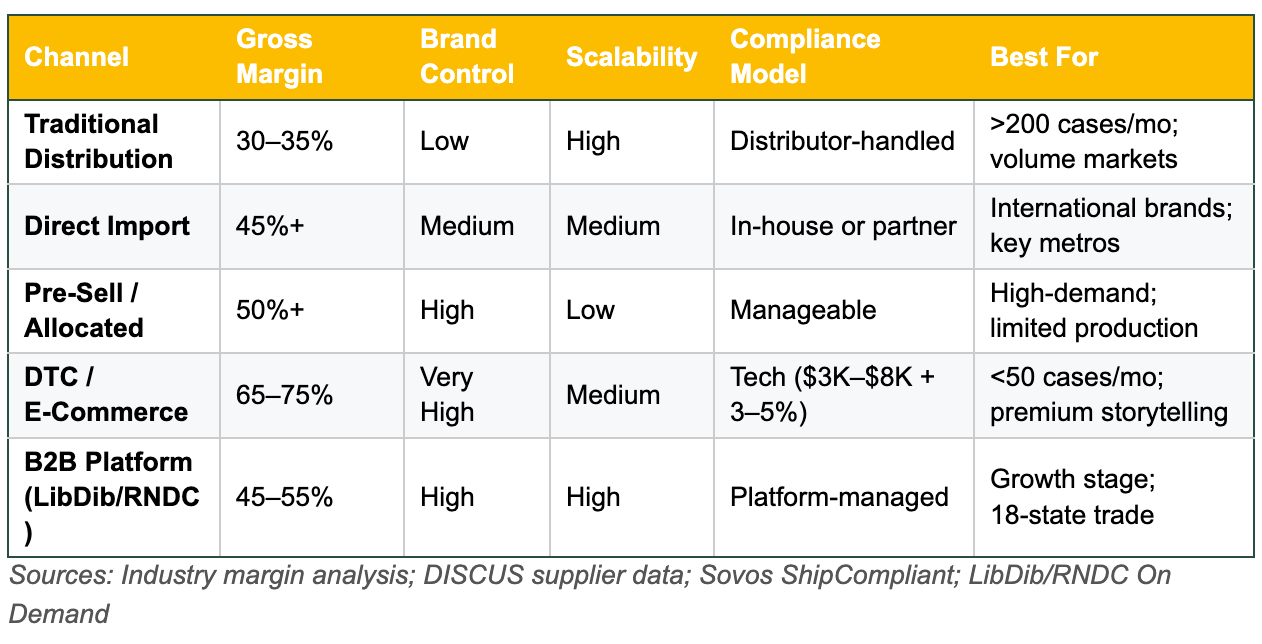

The Margin Math Nobody Does

Wine quantifies the DTC advantage precisely. Gracianna Winery, a 100% DTC boutique producing under 5,000 cases, reports a $68 Pinot Noir nets $61 via DTC versus $34 via wholesale—nearly 80% more. Silicon Valley Bank’s 2025 report: the average winery earns 70% of revenue from DTC. Premium producers average 80%. Wineries above 70% DTC grew fastest; those below 40% saw double-digit volume declines.

For a brand doing $500,000 in annual DTC revenue, the math is blunt: technology-enabled compliance costs $15,000–33,000 per year (or as low as $6,000 at Thirstie’s flat rate). The equivalent compliance function embedded in a traditional distributor’s 30–35% margin on that same revenue: $150,000–175,000. That’s $117,000–160,000 in annual margin recapture—capital that can fund product development, customer acquisition, or survival in a declining market.

For investors: the margin recapture from channel diversification is the single clearest near-term value creation lever in craft spirits. It doesn’t require new product launches, price increases, or market expansion—just a more efficient route to the same consumer.

The Compliance Technology Landscape

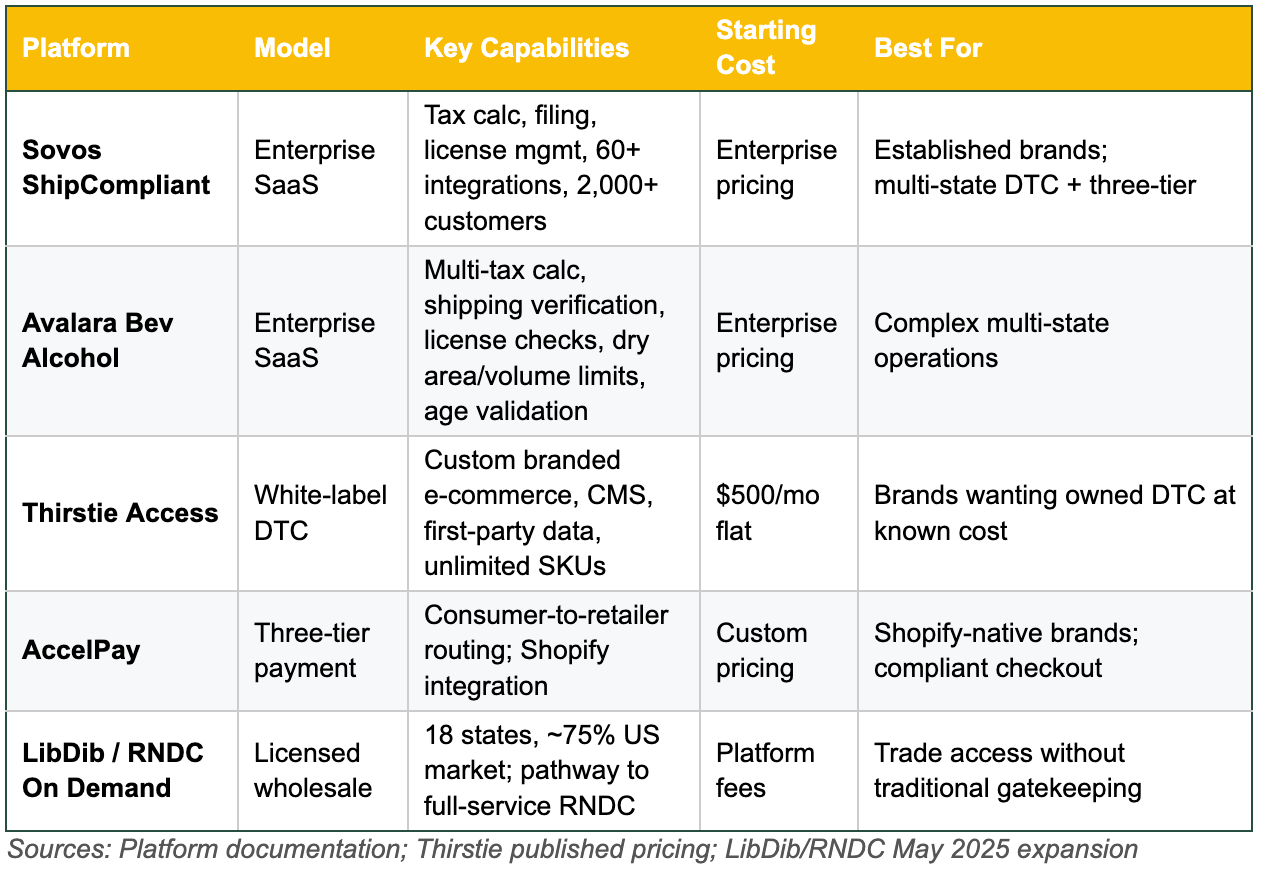

The most persistent myth in spirits distribution is that regulatory compliance is too complex for anything other than a traditional distributor. That was arguably true a decade ago. It isn’t now.

A caveat: a December 2025 industry analysis warned that platforms marketing “commission-free” pricing often carry hidden costs in payment processing margins and volume overrides. Evaluate total cost of ownership, not headline rates.

Fully automated today: multi-state tax calculation, age verification, delivery confirmation, volume limits, dry area checks, and license monitoring. Still requiring human expertise: franchise law navigation (18 states), state label approvals, control state listings, and excise tax edge cases. One development to watch: digital IDs. Georgia confirmed mobile driver’s licenses for alcohol purchases in November 2025—as more states follow, the age verification friction in DTC diminishes substantially.

For operators: the compliance technology stack has crossed the threshold from “interesting experiment” to “mature infrastructure.” The remaining gaps (franchise law, control states) are real but apply to specific market segments, not the entire DTC opportunity. For the growing number of permissive states, the “too complex” objection is outdated.

Case Evidence: What the Transition Looks Like

Napa Valley Distilling

Arthur Hartunian founded Napa Valley Distilling in 2009 after the Great Recession forced him out of insurance. California law didn’t permit distillery direct sales. “We were late on rent, no way to make money… for years I was going door-to-door, trying to sell one bottle at a time.” He became founding president of the California Artisanal Guild in 2011, hired a lobbyist, and helped pass 2013 legislation permitting tastings and limited direct sales. Today the distillery operates primarily DTC—375ml bottles, a tasting room, a cocktail restaurant, retail at Oxbow Public Market. AB 1246 now opens statewide shipping for the market he helped create.

LibDib/RNDC On Demand

As of May 2025: 18 states, ~75% of the U.S. market. RNDC projected $11.4 billion in 2025 revenues. Any permitted producer can list, set pricing, manage trade marketing. Orders fulfilled through RNDC logistics. Jessica Cox of Just Enough Wines: “Our experience with the On Demand model in Texas was instrumental in scaling our presence and ultimately transitioning to full-service distribution.”

Casa Dragones: Category Creation Before Distribution

Co-founded in 2009 by Bertha González Nieves—first woman certified as “Maestra Tequilera”—the brand invested in experiential marketing before pursuing broad distribution. By 2019: 33 U.S. markets. Only then did they sign a national alignment with Southern Glazer’s, expanding to 44 markets from a position of strength. Brands that prioritize category creation over distribution breadth capture 60–70% of consumer price versus 30–40% through distribution-first approaches.

When It Goes Wrong

Westward Whiskey received Diageo’s Distill Ventures investment in 2018. Diageo announced reduced commitments in March 2025. Three weeks later: Chapter 11. By October, original investors acquired the assets. Sales had grown 53% year-over-year—driven by the whiskey club and DTC, which proved to be the resilient core. Separately, Balcones Distillery went from craft darling to Diageo acquisition to halted distilling in August 2025. A distribution consultant captured the generic failure: “Most craft brands treat distributors like taxi drivers. But distributors aren’t in the transportation business. They’re in the portfolio optimization business.”

The pattern across all these cases: the brands that survived disruption—whether regulatory, investor, or market-driven—were the ones with owned customer relationships and diversified channels. The ones that failed had concentrated dependency on a single route to market.

The Concentration Problem

Southern Glazer’s carries over 8,600 brands from ~1,500 suppliers. In beer distribution, the average distributor’s SKU count went from 190 in 1996 to over 1,000 by 2025. The craft spirits data makes this concrete: 90.9% of producers capture only 10.6% of total volume, averaging ~531 cases per year. The 39 largest (1.4%) capture 54.9%.

Craft sales are retreating homeward: home-state share increased 1.1 points since 2021 while out-of-state declined 1.2 points. Producers are pulling back to markets where they have direct relationships. Former ACSA president Becky Harris counted 45 distillery closures since early 2023. In New York alone, 50% of owners surveyed either foresaw closing by end of 2025 or were unsure they’d continue. Average investment per distillery dropped from $337,000 to $289,000 between 2021 and 2024.

Meanwhile, super-premium bottles ($100+) declined nearly 20% since mid-2022. The broader industry posted two consecutive years of declining supplier sales. These closures aren’t driven by bad products. They’re driven by distribution economics that don’t work at sub-scale volumes in a contracting market.

For industry strategists: the current structure concentrates volume in the top 1.4% of producers and leaves 90.9% fighting for scraps of distributor attention. Alternative channels don’t just improve margins—they’re an existential necessity for the vast majority of craft producers who will never generate enough volume to command distributor priority.

The 24-Month Roadmap

Not every brand should abandon traditional distribution. But every brand should audit its options with current data rather than inherited assumptions.

Months 1–6: Foundation

Audit distribution economics. Calculate value-to-cost ratio for every distributor relationship. Deploy compliance technology for at least one direct channel. If eligible for California’s AB 1246 ($125 application, $25–30 annual permit), file now. Same for New York reciprocal shipping. Register on LibDib for trade access across 18 states.

Months 7–12: Build

Launch DTC in every legal state matching your consumer profile. Direct outreach to top 25 on-premise accounts. Track margin capture by channel—this data becomes leverage. Build your email list and membership infrastructure. The Sovos report projects DTC buyers spend $1,484 annually. Wine data shows DTC customers create measurable wholesale lift.

Months 13–18: Optimize

Renegotiate distributor terms using alternative channels as leverage. Shift marketing to owned relationships. Build a membership program—wine data shows 80% club retention versus 30% for one-time buyers. Monitor legislative developments in pending states.

Months 19–24: Scale

Target 50% reduction in traditional distributor dependency by revenue share—not elimination, diversification. Wine’s 92% retail synergy finding confirms that alternative channels create demand that flows through to wholesale. Distributors perform better in retained markets when other channels generate consumer pull.

The Hardware Store Analogy

In 2023, Carlos registered on a digital wholesale platform. Within weeks, he had orders from three states. Within six months, he had direct relationships with a dozen restaurant accounts who’d sought him out because they could actually find his product online. By 2024, his traditional distributor called asking to renegotiate terms—they’d noticed his brand showing up on back bars in markets they thought they controlled.

Carlos told me something I think about often: “It was like I’d been building a house but could only use whatever tools the hardware store decided to stock. Now I can use whatever tools fit my vision. The house I’m building is completely different—and better.”

That’s the shift this article is about. Not abandoning the hardware store. Not pretending it doesn’t sell useful tools. But recognizing that the hardware store’s inventory was never the full set of what was available—and that the brands still limiting themselves to one aisle of one store are the ones running out of time.

The playbook has always existed. The tools have matured. The legal cover is established. The consumer demand is documented. The only remaining variable is whether individual brands choose to act on information that’s been hiding in plain sight—or keep waiting for someone else to build the channel for them.

Building a multi-channel strategy? I’d love to hear what’s working, what’s not, and what nobody told you before you started.