This blog is also available on Substack. Follow along there for addition insights into the artisanal spirits sector and supply chain technology.

TL;DR - The Diffusion Problem

The U.S. just lost its second-largest wine and spirits distributor, not to a competitor but to its own inability to sell. RNDC held the licenses, owned the trucks, and carried the brands, then unwound operations across more than twenty states. At the other end of the same supply chain, the 90.9% of craft producers the ACSA classifies as small average 531 cases a year, with out-of-state volume falling 17.9% annually. Same story, opposite ends: warehousing a brand is not the same as selling it. So brands reach for the next thing, an outside rep, and usually get the same failure at smaller scale, because most independent groups are paid to place a brand, not to build it. On the entire field of players, almost no one is assigned to create demand.

Every founder remembers the day they got distribution. The signed agreement. The first truck. The feeling of having finally arrived somewhere that mattered. For most craft brands, that day is not the finish line they think it is. It is the starting gun on a problem nobody named for them.

In the eighteen months ending June 2026, the United States lost its second-largest wine and spirits distributor. RNDC did not lose to a sharper competitor or a better price. It came apart. Operations in more than twenty states were sold or exited, roughly 4,677 job notices were filed, and eleven markets and some $6 billion in revenue went to Reyes. RNDC held the licenses. It owned the trucks. It carried the brands. What it could not do, at the scale its margin promised, was sell them.

That is not a distribution failure. It is a category error the industry has made for seventy years, treating one company as if it performed two completely different jobs. This piece is about the gap between those jobs, the players who are supposed to fill it and mostly do not, and why 2026 is the year the gap stopped being invisible.

Two Ends of One Story

Stand at the other end of the same supply chain and you see the mirror image. The American Craft Spirits Association’s 2025 Craft Spirits Data Project found that the small producers who make up 90.9% of the craft universe move an average of 531 cases a year. Not their breakout brands. The median reality.

Look closer and the diagnosis sharpens. Those same small producers sell just 5.5% of their volume outside their home state, and that out-of-state business is shrinking at a 17.9% compound annual rate. The home market holds. The distributed market, the one that supposedly justifies signing a distributor, is evaporating.

Put the two ends together and a single picture emerges. A national distributor collapsed because it could not monetize selling. Thousands of small brands are going quiet in distribution for the same reason, one warehouse at a time. The distributor’s failure made headlines. The brand’s failure makes none. It just shows up as a reorder that never comes.

For brands: the question to ask about any distribution agreement is not “are they moving cases?” It is “is anyone actually selling this, and can I see the evidence?”

The State of Sales

Here is the part nobody maps. Before you decide who should be selling your brand, look at who is actually on the field.

Start with the labor market, because it tells the whole story in two numbers. The industry now supports roughly 9,000 fractional sales professionals charging an average of $11,732 a month to build the commercial muscle most brands never built in-house. The 90.9% of craft producers moving 531 cases a year are exactly who needs them, and the last who can afford them. That gap is the state of sales.

The macro picture around that gap is not friendlier. U.S. spirits supplier sales hit $36.4 billion in 2025, down 2.2%, with value falling while volume held, the signature of consumers trading down. The middle tier, meanwhile, has thinned to a near-duopoly in the states that matter. After the RNDC dissolution, Reyes alone now reaches 52% of the legal-drinking-age population, and several large states are effectively down to two distributors a brand can sign. That is fewer doors to knock on, not more. The one bright line runs through the bar: on-premise spirits gained share in 2025, reaching 46.9% of on-premise spending, even as off-premise volumes fell. The channel that is growing is the one place human selling still decides the outcome.

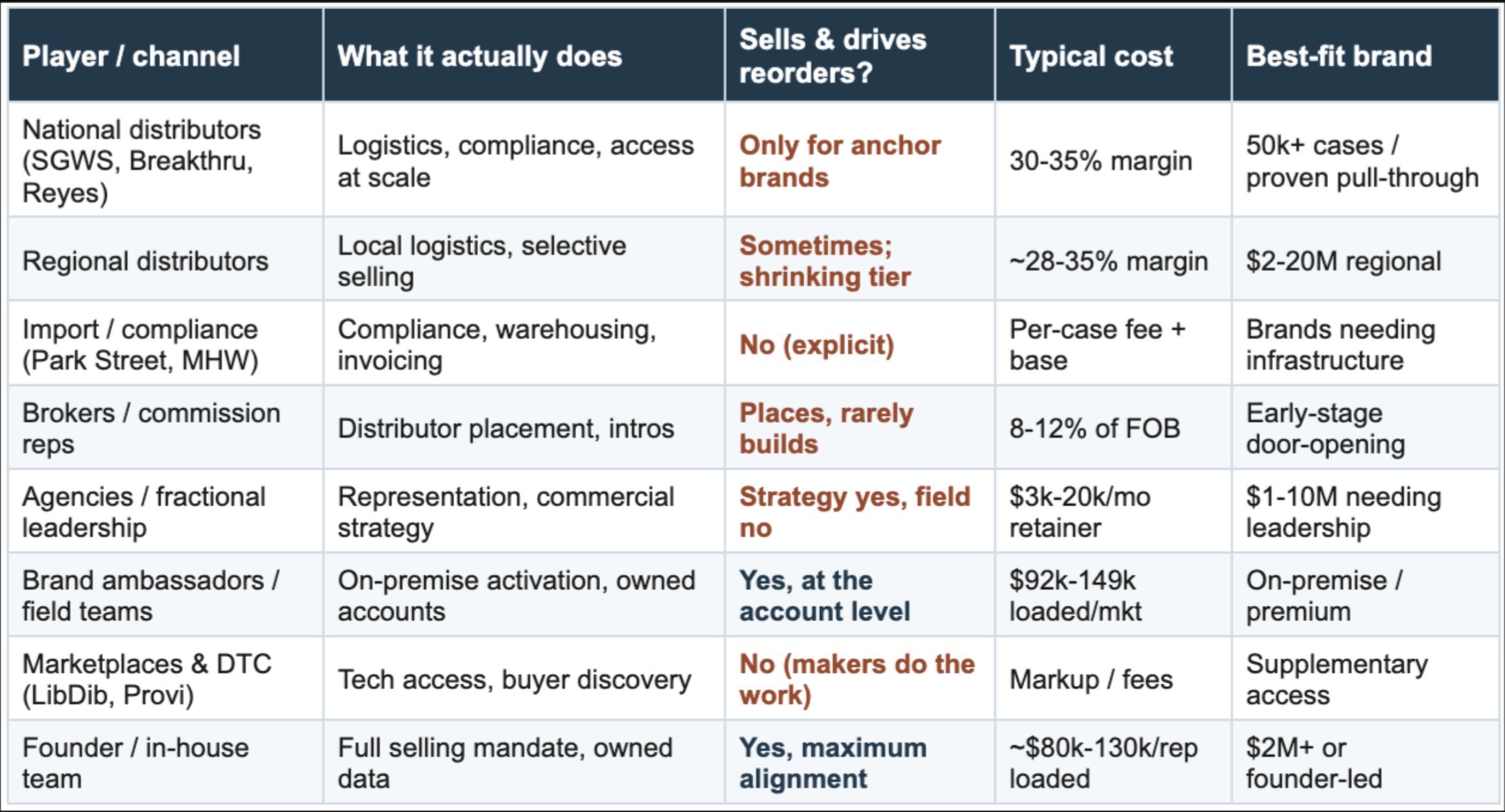

Now the map itself. Every player below does something real. Read down the column that matters, though, the one that asks whether they sell your brand and drive reorders, and the answer is almost always no, only for anchor brands, or the maker does the work.

The table makes a point prose cannot. There is no row whose job is to create demand for a brand the market has never heard of. The distributor moves it. The importer keeps it compliant. The marketplace lists it. The platform measures it. Each assumes someone else is doing the selling. For a small brand, that someone is usually no one.

For operators: unassigned work does not get done. If no line on this map is paid to create demand for your brand, the default outcome is dormancy, not growth.

Registration Is Not Velocity

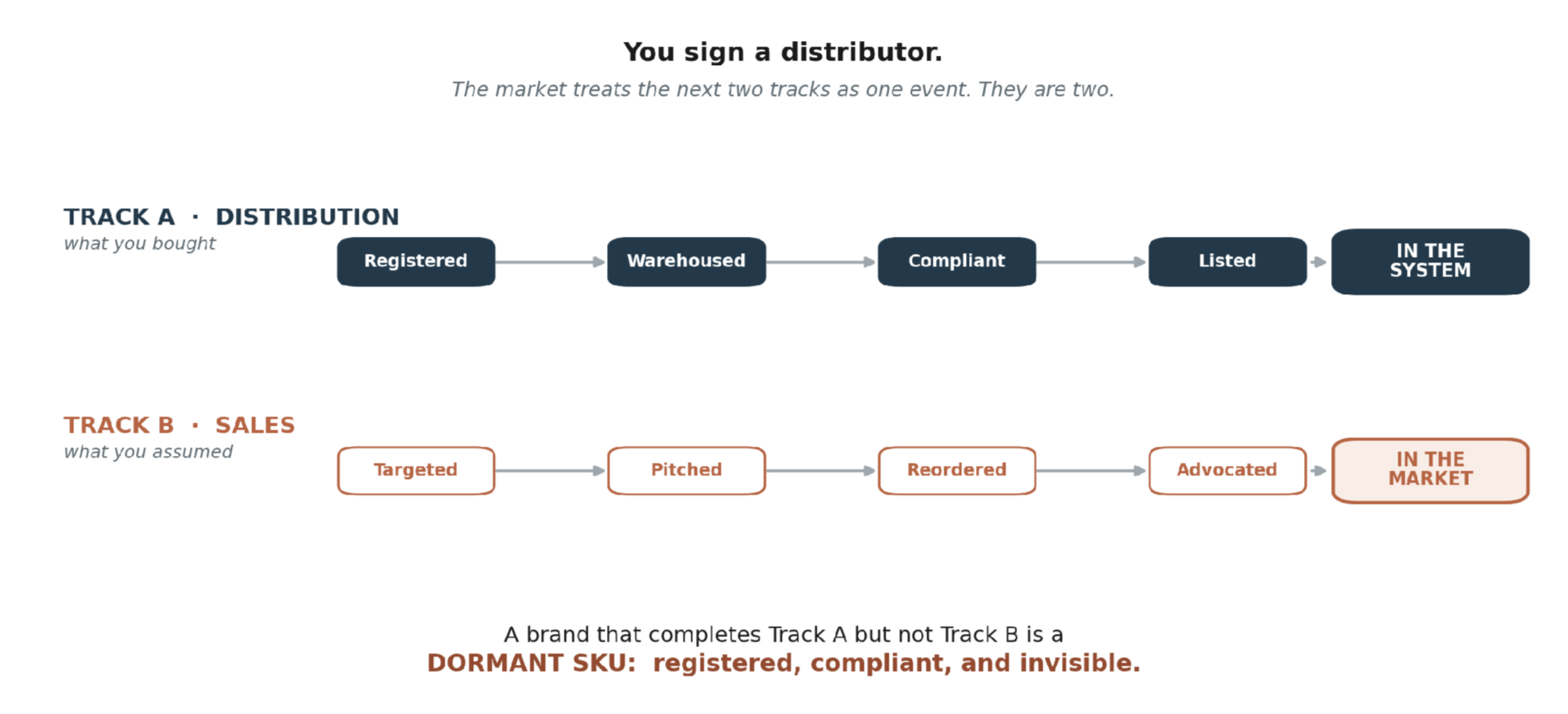

Here is the confusion at the heart of it. The industry treats “getting into distribution” and “getting sold” as the same event. They are not even close.

Getting into distribution is an administrative achievement. Your brand is registered, your product is warehoused, your compliance is clean, your SKU is listed. Getting sold is a human achievement. Someone targets the right accounts, pitches a buyer, earns the reorder, and becomes the face of the brand in a market that has never heard of it. The first is paperwork. The second is work.

Software people have a name for this gap. A user who signs up and never opens the product again is “signed up but not activated.” The onboarding succeeded; the usage is zero. A brand that completes every step of distribution and never gets sold is the exact same animal. The logistics happened. The activation never did. Retail calls its version a zombie SKU; marketplaces call it dark inventory. Spirits has lived with the condition for decades without naming it, so let’s name it: the dormant SKU.

A dormant SKU is not a brand that failed in the market. It is a brand that was never actually taken to market. Registered, compliant, and invisible, sitting in a warehouse waiting for calls that were never anyone’s job to make.

For operators: if you cannot see your own depletions by account this week, you are not managing velocity. You are waiting to discover its absence, usually a quarter too late to fix it.

You Paid Full Freight for Half the Service

None of this would matter if selling came free with the freight. It does not, and increasingly it does not come at all.

A distributor’s margin runs 30 to 35% of the wholesale price. Historically that number bought three things bundled together: shelf placement, buyer education, and ongoing reorder management. The first is logistics. The second and third are sales. Practitioner reporting through 2026 describes a tier that has quietly redefined itself around the first and shed the rest, delivery-and-billing operations that kept the full margin while gutting the selling function. So you pay the 30 to 35% for logistics, and then you pay again, for a rep or an ambassador, to do the selling the margin was supposed to cover. You are double-paying for distribution. You paid for sales twice and own it once.

If that reads like a small brand’s complaint, consider who else figured it out. When Sazerac, one of the largest spirits companies on earth, left RNDC, it stated in its 2023 complaint that the distributor had “refused to invest in its salesforce,” and that Sazerac had spent nearly $100 million building its own field marketing team to do the selling itself. RNDC countersued, arguing Sazerac was pulling distributor functions in-house in ways that strained the three-tier rules, so treat the figure as Sazerac’s own characterization, not a settled fact. To be fair, this is not universal. A distributor will genuinely sell a brand that already shows pull-through, because that brand earns a rep’s commission. The failure lands on everyone below that line, which is to say the bottom 80 to 90% of craft brands by volume. But sit with the core admission. If a company that size concluded its distributor was not selling and built a nine-figure sales operation to compensate, what exactly do you think your distributor is doing for your three pallets?

For investors: a brand whose only sales engine is a line item in a distributor’s margin owns no sales capability. It has rented one, from a landlord with thousands of other tenants and no obligation to grow any of them.

So You Hire Feet on the Street

When the distributor does not sell, every brand reaches for the same thing next: an outside rep, a broker, a “feet on the street” arrangement to make something happen in the market. Most are disappointed, and in my experience the disappointment is structural, not personal. The reps are not lazy. The model is built to fail the small brand.

Three forces do the damage. The first is broker bloat. A commission rep carrying twenty or thirty lines faces the same incentive geometry as a distributor rep carrying 280: time spent on your brand is time not spent on a brand that pays faster. Your low-volume label loses that contest every week. The second is adverse selection. A commission-only deal with no retainer attracts two kinds of rep, the rare one with deep current relationships who does not need a guarantee, and the one who cannot command a retainer because the relationships are not there. The brand that can only afford commission gets the second kind at disproportionate rates. The third is the incentive itself. A rep who places you with a distributor and earns on the first shipment has satisfied most agreements, even if you go dormant the next quarter. The pay is for placement, not for building.

This is not an argument against outside help. It is an argument about structure. The same table shows when outside selling actually works, and the pattern is consistent: an established brand moving proven velocity into a new geography, a brand with documented pull-through using a rep to open doors, or fractional leadership that manages distributors and strategy rather than personally working accounts. In each, the rep is paid to build or held to a number, not paid to place and disappear. That distinction, paid-to-build versus paid-to-place, is the whole game.

For brands: hiring a rep does not solve dormancy. It relocates it, from distributor inaction to broker bloat, unless the arrangement is paid to build and held to a velocity number you can see.

The Stakes Just Went Up

Dormancy in a rising market is a missed opportunity. Dormancy in this one is a slow death.

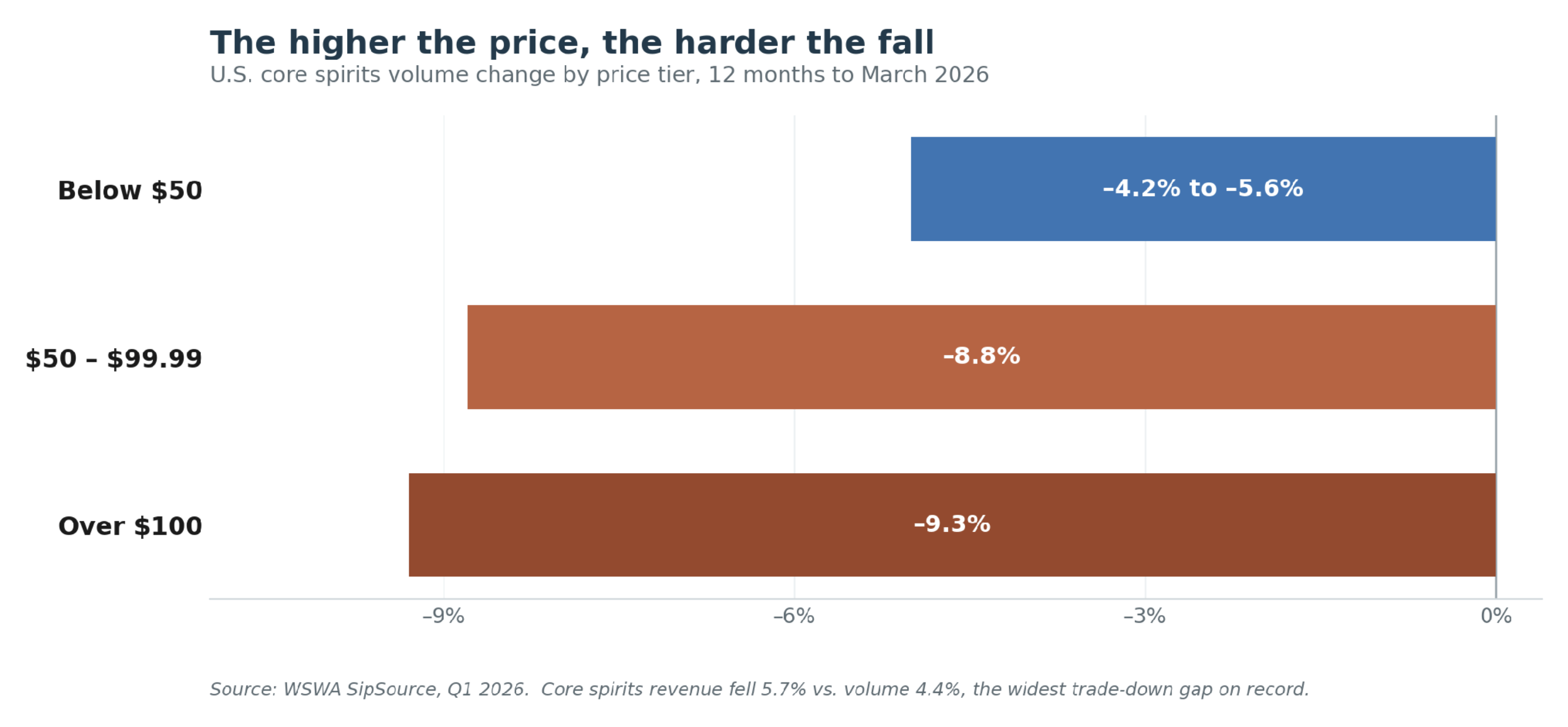

The most recent SipSource data from the wholesalers’ association shows core spirits volume down 4.4% and revenue down 5.7% in the twelve months to March 2026, a 130-basis-point gap that is the widest on record and the clearest signal yet that consumers are not just drinking less, they are trading down. The pressure lands hardest exactly where artisanal brands live. Bottles priced $50 to $99.99 fell 8.8%; bottles over $100 fell 9.3%; the cheapest tiers fell least. The higher the price, the harder the fall.

For agave, the category many of these producers call home, volume slipped about 3% and revenue about 6.6%, value falling faster than volume, the trade-down written into a single category. Read it together and the conclusion is uncomfortable. The brands paying the most for distribution are losing demand fastest, at the precise moment their distributor’s selling function is thinnest and the outside reps they hired are working someone else’s faster-paying line. A dormant premium SKU in a depremiumizing market is not waiting to wake up. It is waiting to be discontinued.

For brands: in a soft market, the active sales advocate is not a luxury you add after you scale. It is the thing that decides whether you get to scale at all.

Dormancy Used to Be Invisible. That Excuse Is Gone.

For most of the three-tier era, a brand could not see its own dormancy until the quarter was already dead. Depletion reports arrived monthly, if at all, and by the time the numbers showed a stall the inventory had aged on a shelf two states away.

That changed. A new class of depletion analytics now flags a velocity drop within hours of it happening at a specific account, and surfaces the tell that used to hide in plain sight: shipments holding steady while depletions slow, the signature of reorders quietly drying up. The tooling will not sell the brand for you. But it ends the era when “I didn’t know it had stalled” was a defensible answer. Dormancy is now a measurement you can take. The only question is whether you are taking it.

When the trucks stopped in California, the brands that came through it cleanest were not the ones with the best distributor. They were the ones who already knew, by name, the buyers reordering their product, because someone on their own side had been in those accounts all along. The brands that struggled had a different morning: refreshing an inbox, waiting on the transfer of a relationship they assumed they owned, and discovering it had never been theirs to transfer.

By now you have tried two things the market sold you as a sales function. You signed a distributor and learned it moves boxes. You hired a rep and learned most are paid to place, not to build. Neither was built to be the thing you needed. So Part 1 leaves you with a single question, and it is worth answering honestly before the next distributor decides to exit your state: if your distributor and your broker both disappeared tomorrow, would you know who is actually buying your brand, or only where it is parked, and who you would have to pay, again, to find out?