This blog is also available on Substack. Follow along there for addition insights into the artisanal spirits sector and supply chain technology.

It’s like paying a 20% convenience fee every time you use an ATM—except the fee is hidden in the exchange rate, the processing time, and the fine print. And you’ve been paying it so long you forgot there was ever another way.

I’ve spent years working with spirits suppliers—producers, brand owners, and portfolio operators alike—watching them pour everything into perfecting their craft and market positioning. They obsess over liquid quality, debate brand architecture, and lose sleep over distribution strategy. Yet most have no idea that somewhere between 15-25% of their potential value disappears before their product ever reaches a consumer’s lips.

This isn’t a metaphor. It’s a quantifiable tax hiding in plain sight—buried in compliance timelines that should take weeks instead of months, in service fees that compound at each tier, in operational blind spots that everyone accepts because “that’s just how things work.”

Here’s what industry veterans know but rarely discuss openly: the inefficiency persists not because solutions don’t exist, but because the people who could fix it profit from complexity.

Below, I provide a framework for identifying where you’re bleeding value and what to do about it—whether you’re running a single-brand operation or managing a multi-SKU portfolio across markets.

The Anatomy of the Invisible Tax

Before we can fix anything, we need to see it clearly. The value drain happens across four distinct channels, each compounding the others.

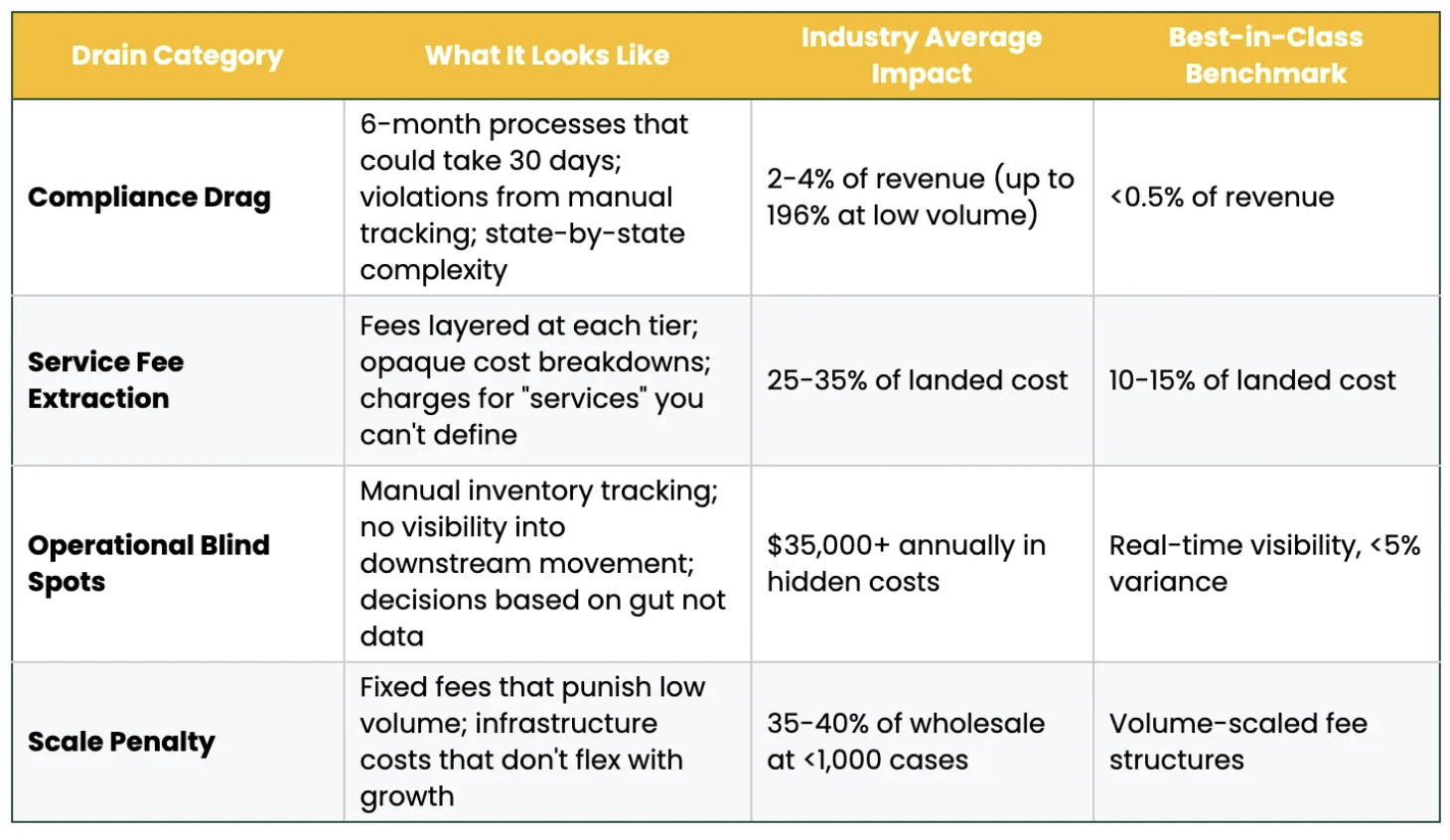

The Four Drains: Where Your Margin Disappears

The cumulative effect? A $65 premium spirit loses $9.75 to $16.25 in value before the first sip—and most suppliers can’t tell you exactly where it went.

Who Benefits from Complexity

Here’s where the analysis gets uncomfortable for the industry.

Between 1998 and 2020, the alcohol industry spent $541 million on federal lobbying:

- 90% came from the largest market-share companies

- Four organizations account for over half of all spending

- 43% of alcohol lobbying comes from trade associations—the highest of any industry studied

The tell that reveals the strategy? Connecticut wholesalers spend twice as much on lobbying as California wholesalers, despite serving one-tenth the population. That pattern suggests lobbying intensity correlates with protecting regional positions, not serving market needs.

The three-tier system multiplies this effect. What started as post-Prohibition consumer protection has evolved into a complexity multiplier that:

- Penalizes scale economies for emerging suppliers

- Protects margins for established players

- Creates information asymmetries that benefit intermediaries

Academic research found that even when multiple wholesalers sell identical products, pricing regulations create monopoly-level pricing through game theory dynamics. Distributors capture price-cost margins around $3 per liter—but actual profit margins are only 1.8%.

This structural protection comes at a cost the industry can no longer hide: Between August 2024 and August 2025, active craft distilleries dropped 25.6%—from 3,069 to 2,282 operations. The brands paying the invisible tax without measuring it are funding the consolidation wave that will acquire them at distressed valuations.

Where does the gap go? Into operational bloat that incumbents have no incentive to eliminate. You’re not paying for service. You’re subsidizing inefficiency.

The Scale Penalty: Understanding Your Position

Every supplier operates within a volume range that determines their negotiating leverage, service options, and fee burden. Understanding where you sit—and what it costs you—is step one in any optimization strategy.

The math is brutal in the middle ranges.

At 12,000 cases? That same compliance burden drops to 3.8-9.8% of revenue. Same costs—spread across volume that makes them manageable.

Key insight for portfolio operators: Managing multiple brands doesn’t automatically improve your position if each brand operates independently. Consolidated compliance, shared logistics, and coordinated market entry can capture scale benefits even with smaller individual SKUs.

What Services You Actually Need (And When)

Not every supplier needs every service. The mistake many operators make is either over-investing in infrastructure too early or under-investing until compliance violations force their hand.

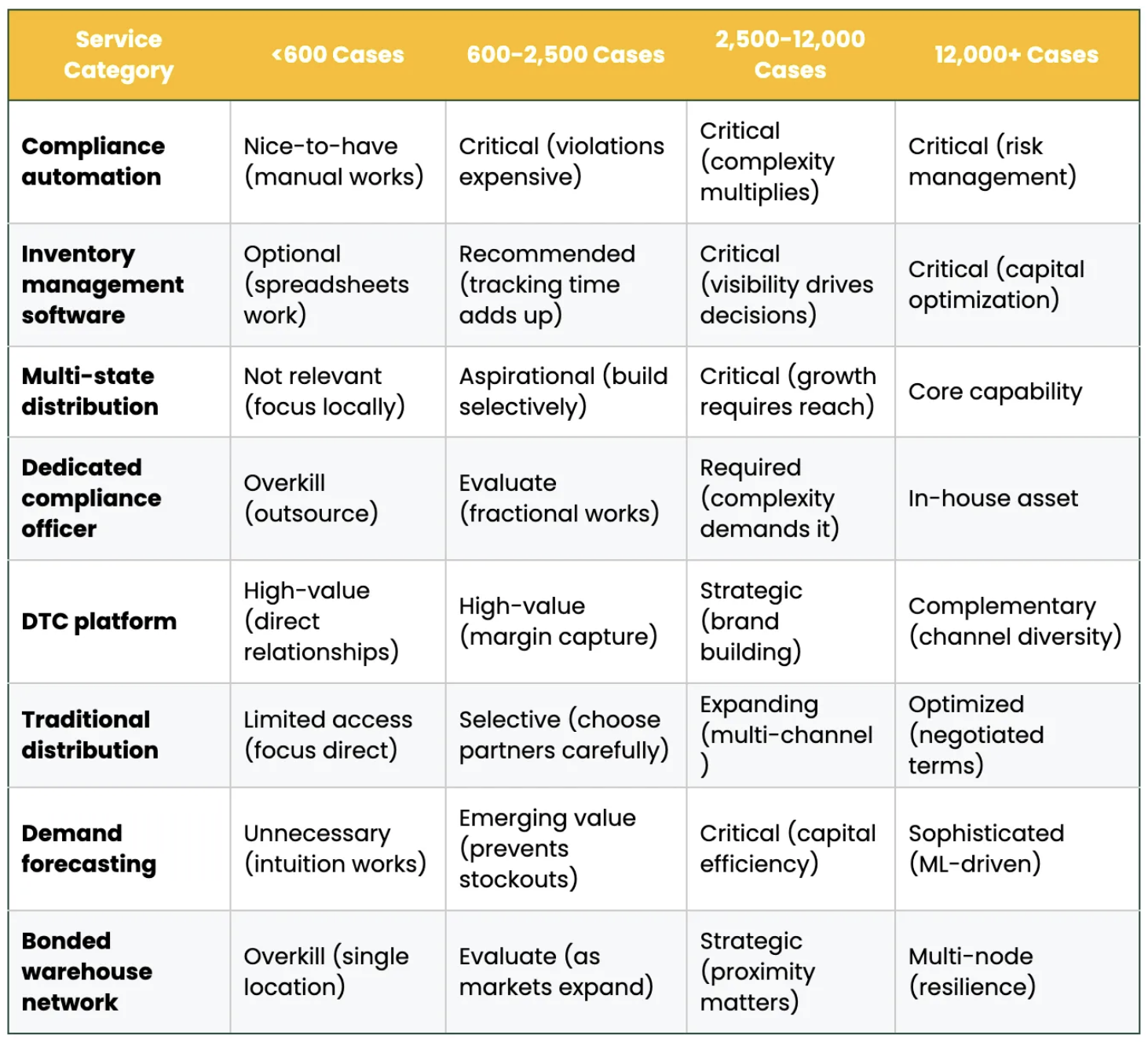

Service Necessity Matrix by Scale

The expensive mistake: Purchasing enterprise-grade infrastructure at startup volumes. A $50,000 ERP system doesn’t help a 500-case operation—it just accelerates cash burn.

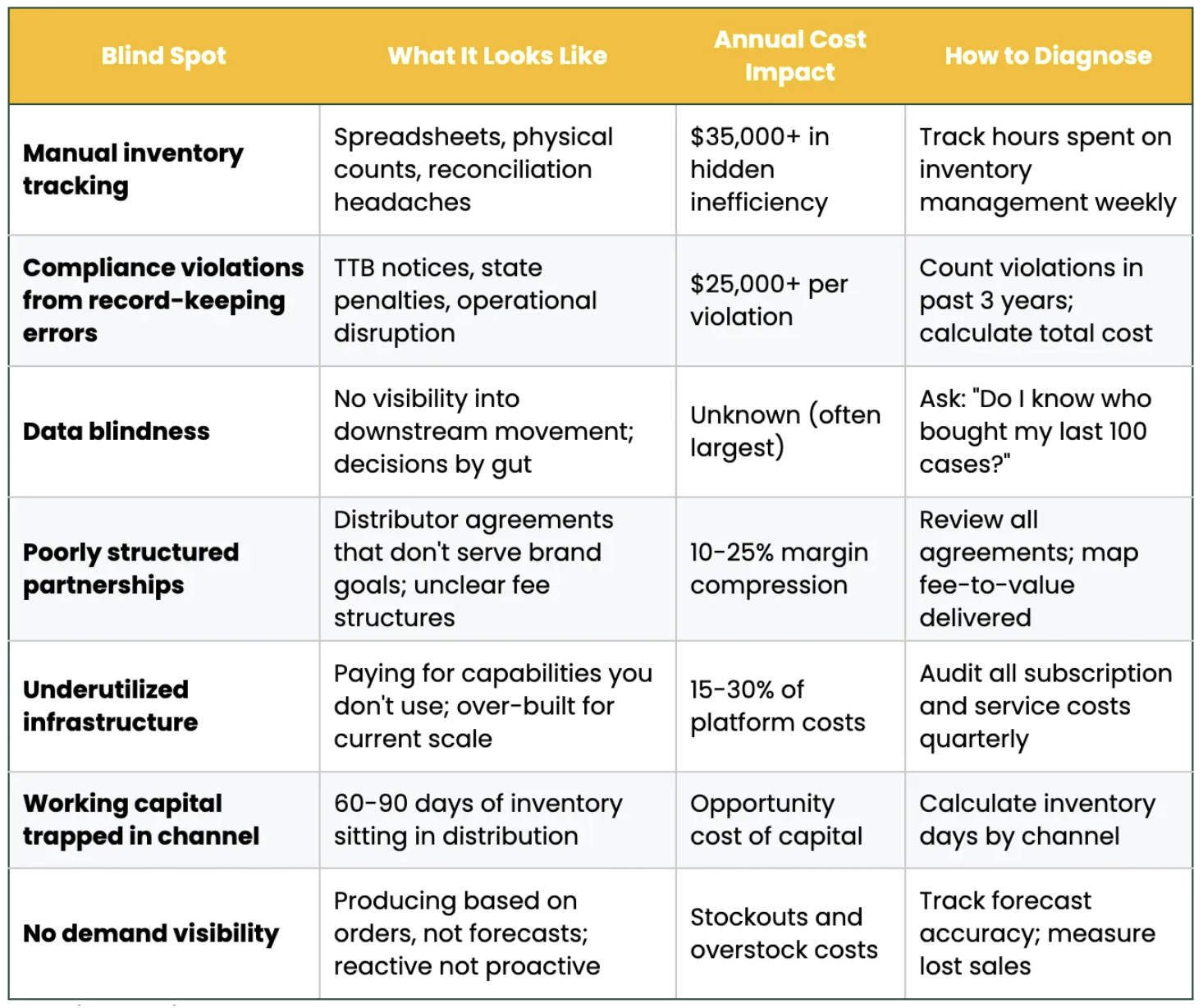

The other expensive mistake: Staying on spreadsheets at 3,000 cases because “it’s always worked.” The 89% of craft distilleries still using manual inventory management lose an average $35,000 annually to inefficiencies they can’t even measure.

Platform Types: What’s Actually Useful at Your Scale

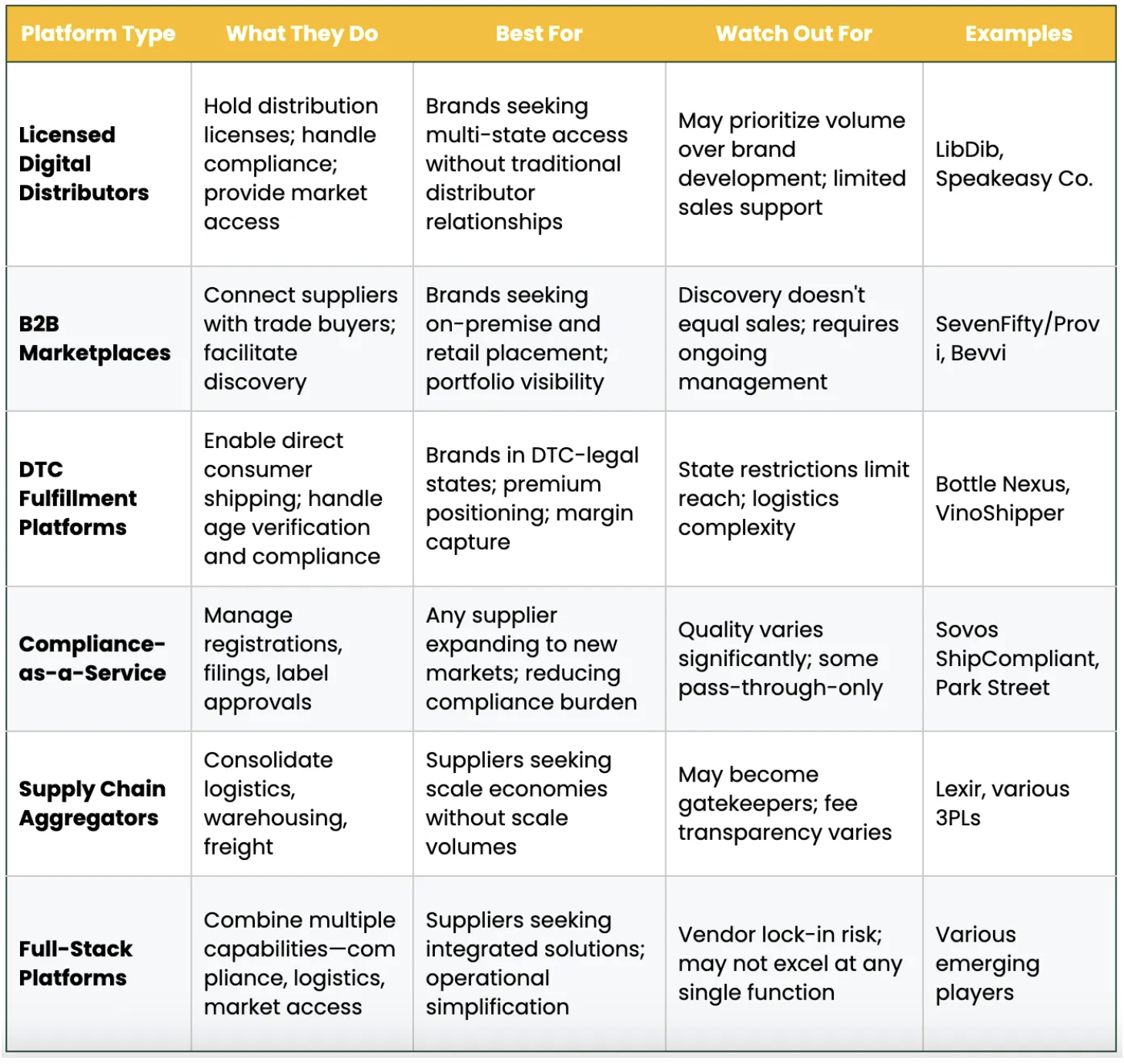

The beverage industry has spawned dozens of platforms promising to solve distribution, compliance, logistics, and market access challenges. Not all deliver equal value at every stage.

Platform Taxonomy for Spirits Suppliers

Platform Selection Framework:

- Match platform capabilities to your actual gaps. If your bottleneck is compliance, a marketplace won’t help.

- Understand fee structures before committing. Some platforms take transaction fees; others charge subscriptions; many do both.

- Evaluate what you’re giving up. Customer data? Pricing control? Brand presentation?

- Check for scale alignment. Platforms optimized for high-volume suppliers may ignore sub-1,000 case brands.

- Ask about switching costs. Integration with existing systems matters less than ability to leave if needed.

The uncomfortable truth about platform fees: Every platform extracts value. The question is whether they create more value than they capture—and whether that equation changes as you scale.

The Self-Inflicted Wounds: Where Operators Hurt Themselves

While regulatory capture explains external extraction, suppliers are also bleeding value through their own operational gaps. This isn’t about judgment—it’s about visibility.

Common Blind Spots Across Supplier Types

The diagnostic that matters most: Can you answer these questions in under 5 minutes?

- What’s your true all-in cost per case across all channels?

- Which of your SKUs generates the highest margin after all fees?

- How many days between production and cash collection?

- What percentage of your retail price do you actually capture?

If these require digging through files and making calls, you have a visibility problem that’s costing you money.

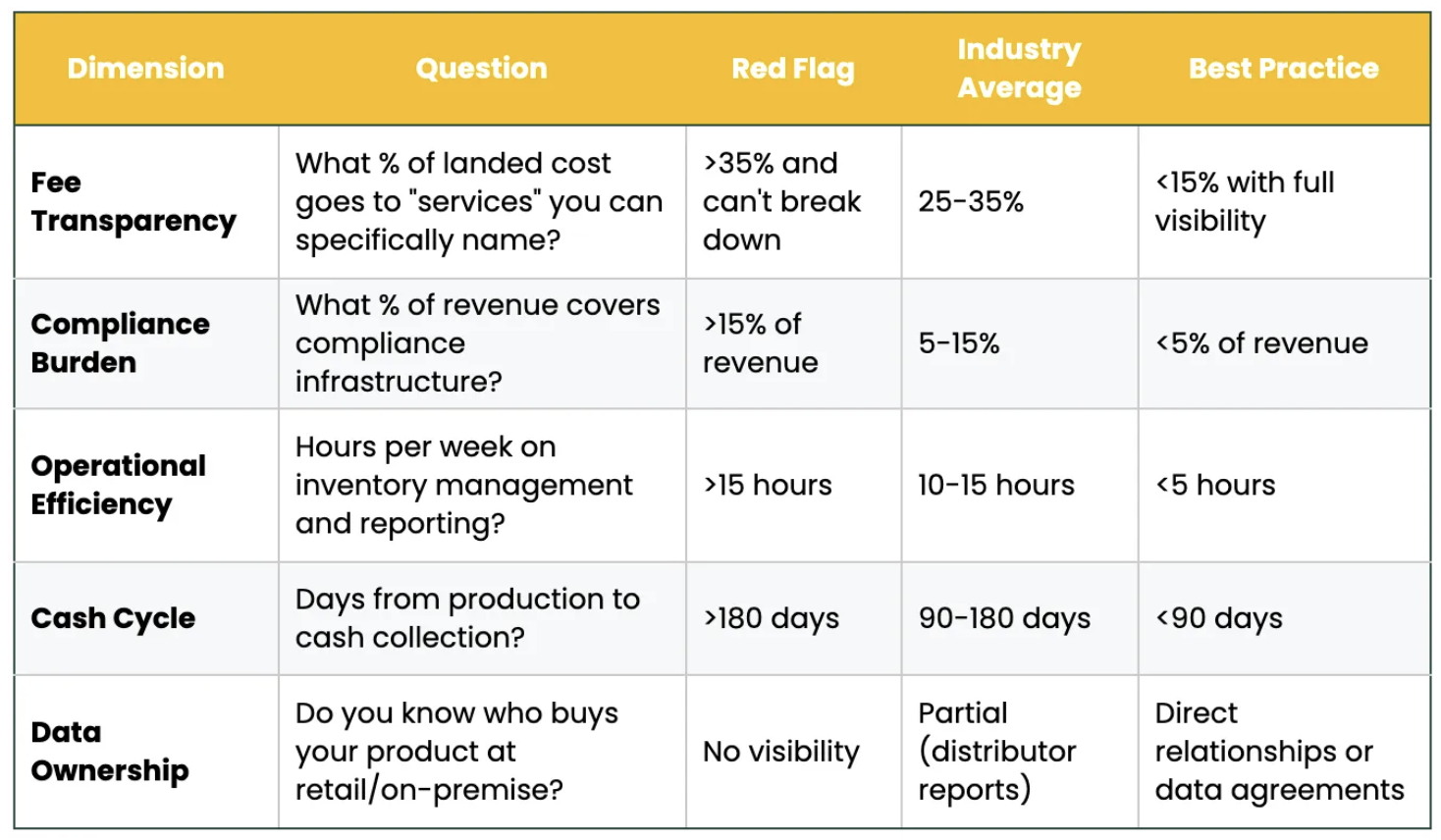

The Self-Audit Framework: Quantify Your Exposure

Use this framework to assess where your operation stands and where to focus improvement efforts.

The Five-Dimension Assessment

Scoring your position:

- 0-1 dimensions at “Best Practice”: Significant optimization opportunity exists

- 2-3 dimensions at “Best Practice”: Targeted improvements available

- 4-5 dimensions at “Best Practice”: Focus on maintaining advantage

Questions to Ask Your Service Providers

These questions expose whether you’re getting value or subsidizing someone else’s inefficiency.

For distributors and importers:

- “What percentage of other clients my size are you serving, and at what fee structure?” (Exposes if you’re subsidizing larger accounts)

- “Show me the cost breakdown: what’s your margin vs. pass-through costs?” (Tests transparency)

- “At what volume threshold do terms improve, and by how much?” (Quantifies the scale penalty)

For platforms and technology providers:

- “What data do I own, and what data do you retain if I leave?” (Clarifies lock-in risk)

- “What’s the average time for suppliers my size to see ROI?” (Forces specificity)

- “Can I speak with three clients who left your platform?” (The question they won’t expect)

For compliance services:

- “What’s your violation rate among clients you’ve managed for 2+ years?” (Tests actual effectiveness)

- “If I grow 3x, how does pricing change?” (Reveals scale alignment)

- “What operational efficiencies have you helped similar clients achieve?” (Moves beyond pass-through)

The response that should concern you: Any version of “it’s complicated” or “every client is different” when asked about fee structure or performance metrics.

Strategic Pathways by Scale

Strategic Pathways by Scale

There’s no universal playbook. Your optimal approach depends on your current position, available capital, and strategic objectives.

For sub-600 case suppliers:

Focus: Maximize direct relationships; minimize intermediary layers; build brand equity before scaling distribution.

- DTC in legal states captures 70-80% of consumer price vs. 27% through traditional distribution—yet spirits DTC remains blocked in 46 states

- On-premise and tasting room create high-margin, high-relationship revenue

- Keep infrastructure lean; outsource compliance as needed

- Avoid the death valley trap of expanding before building sustainable economics

For 600-2,500 case suppliers (the danger zone):

Focus: Either scale quickly through the vulnerable middle or optimize for profitability at current volume.

- The math says you’re paying 28-38% premium for being between bootstrapping and scale

- Calculate capital needed to reach 12,000+ case threshold; model timeline realistically

- If scaling isn’t viable, optimize for margin at current volume rather than chasing growth that compounds losses

- Select platforms and partners based on your actual strategy, not aspirational positioning

For 2,500-12,000 case suppliers:

Focus: Build infrastructure that scales; negotiate from emerging leverage; develop data capabilities.

- You’re approaching territory where negotiated terms become possible

- Invest in visibility systems that inform better decisions

- Consider platform solutions that grow with you rather than require replacement

- Map multi-channel economics; understand which channels serve which objectives

For 12,000+ case suppliers and portfolio operators:

Focus: Optimize across channels; leverage scale for negotiating power; build proprietary data advantages.

- You have options—exercise them

- Benchmark fee structures against industry alternatives

- Build direct relationships where regulations permit

- Use data as competitive advantage, not just operational necessity

The 15-25% invisible tax is real. It’s quantifiable. And it’s a choice.

Think of it like the travel industry transformation. Twenty years ago, booking international travel required agents, brokers, multiple phone calls, and significant fees at each step. Someone extracted value at every handoff. Now you book on your phone in minutes, often directly with providers.

The travel agents didn’t disappear because consumers stopped wanting to travel. They became obsolete because the value they extracted exceeded the value they created.

The artisanal spirits supply chain is approaching a similar inflection point. The question isn’t whether the invisible tax will be disrupted—it’s whether you’ll be among those capturing the efficiency or those subsidizing it until you can’t anymore.

The suppliers who thrive aren’t those blindly following either traditional or alternative distribution dogma. They’re those who:

- Know their true all-in costs with granular precision

- Match service providers to actual needs, not aspirational scale

- Build visibility systems that inform better decisions

- Regularly audit partnerships for value-to-fee alignment

- Recognize that complexity often protects someone else’s margin, not their own

Start measuring. Start asking uncomfortable questions. Start architecting around a system designed for someone else.

Because the 15-25% you’re paying without knowing it? That’s your margin, your growth capital, your resilience.

It’s time to take it back.