This blog is also available on Substack. Follow along there for addition insights into the artisanal spirits sector and supply chain technology.

TL;DR

The U.S. three-tier system is undergoing its most significant structural shift since Prohibition. California opened DTC spirits shipping to 39 million residents in January 2026. Wine DTC now covers 48 states; spirits are on the same trajectory. The FTC is suing the nation’s largest distributor for pricing discrimination—and the case survived a motion to dismiss under a new administration. Both major distributors now formally recognize a digital B2B platform as a legitimate ordering channel after settling an antitrust lawsuit. Consumer demand for DTC spirits is documented and overwhelming (67–84% want access). The regulatory barriers most brands cite aren’t legal barriers—they’re assumptions. This article maps the five structural forces proving the system is more navigable than the industry believes.

Everyone talks about the three-tier system like it’s the Berlin Wall—an impenetrable barrier dividing producers, distributors, and retailers with no crossing permitted. But if you look at what’s actually happening in early 2026, the analogy is wrong. The three-tier system is more like airport security: structured, regulated, sometimes frustrating—but designed to be navigated by anyone who understands the rules.

The gap between perception and reality is costing brands 15–20% of margin they could be capturing. And the urgency is real: the ACSA CEO called 2025 “the most challenging year yet for craft spirits producers.” The 2025 Craft Spirits Data Project counted 2,282 active distilleries, down from 3,069 a year earlier. Craft spirits volume dropped 6.1% in 2024 while the broader market posted its second consecutive year of declining supplier sales, falling to $36.4 billion in 2025.

This article maps the structural forces creating opportunity for brands willing to look. A companion piece covers the economics and implementation.

The Decade Spirits Lost

U.S. spirits supplier sales totaled $36.4 billion in 2025, per DISCUS. The broader consumer market exceeds $100 billion. Yet online beverage alcohol penetration sits at roughly 3.5% of total value, according to IWSR’s 2025 E-Commerce Strategic Study. Overall U.S. retail e-commerce: approximately 22%.

That’s not slightly behind. That’s a full decade of unrealized potential.

The consumers who buy spirits online are different from their in-store counterparts. Average order values run $150–200—roughly double the $75–100 typical in retail. The 2025 Sovos ShipCompliant/ACSA report projects likely DTC buyers would spend $1,484 annually. Premium products account for 40% of online sales but 60% of revenue.

IWSR’s revised forecasts project 3% compound annual growth through 2029, with sharp divergence by channel: on-demand delivery at +8% CAGR, omnichannel at +3%, marketplaces at +2%, and DTC flat globally. But the global figure masks the U.S. spirits-specific trajectory, which is expanding legislatively into new states. Category dynamics reinforce this: agave spirits project +5% CAGR in online value, outpacing American whiskey (+3%) and Scotch (+1%). The categories with the strongest cultural narratives perform best in digital channels.

For brands and investors: the 3.5% vs. 22% gap represents a multi-billion-dollar market that exists in virtually every other retail category but hasn’t been built in spirits. The constraint has been regulatory, not demand. That regulatory picture is shifting now.

The Post-Drizly Landscape

Drizly’s shutdown in March 2024 eliminated the industry’s dominant e-commerce platform overnight. At its peak: 41.2% of purchase intent clicks, 100+ million customer reach, 1,400 cities, ~4,000 retail partners, $1.17 billion in 2020 sales. Uber’s $1.1 billion acquisition ended in a near-total write-off—Drizly had been valued at $73 million just four years earlier.

The market has permanently fragmented. Instacart leads with 40.3% of purchase intent clicks, followed by Total Wine (24.3%), Walmart (22.9%), Minibar (8%), and Kroger (4.5%). As Rabobank analyst Bourcard Nesin put it: “Nearly half a billion dollars in online alcohol sales disappeared overnight.” No single platform has replicated Drizly’s alcohol-specific dominance.

Some independent retailers migrated to white-label solutions like City Hive. Others abandoned e-commerce entirely. The brands that maintained direct customer relationships alongside marketplace presence absorbed the disruption. The ones that hadn’t scrambled.

The Drizly shutdown is a case study in platform dependency—the same structural risk that makes exclusive distributor dependency dangerous. The lesson applies regardless of channel: any brand whose primary route to market runs entirely through infrastructure it doesn’t control is one business decision away from losing access.

The DTC Legislative Wave

As of January 2026, nine states plus D.C. permit interstate DTC spirits shipping—compared to 48 states plus D.C. for wine (Mississippi became the 48th in July 2025). The gap is enormous. It’s also closing faster than most people realize.

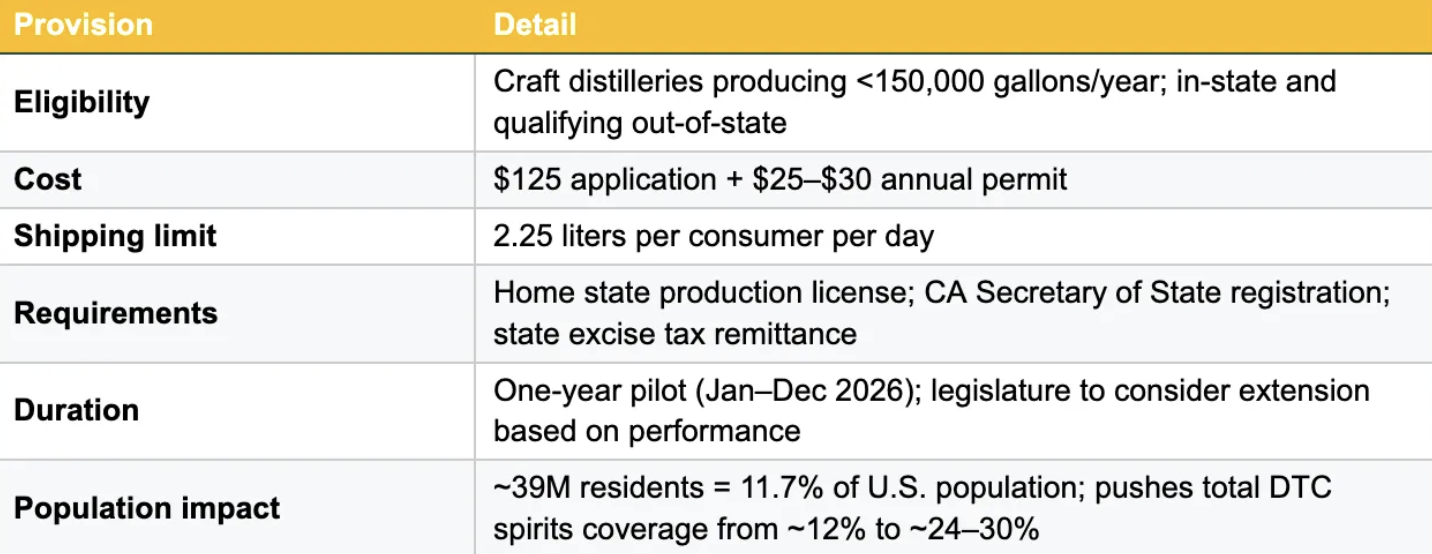

California AB 1246: The Bellwether

Governor Newsom signed AB 1246 in October 2025, creating a one-year pilot effective January 1, 2026:

Source: Sovos ShipCompliant analysis; Clark Hill legal review

This is the single largest DTC spirits market access event in U.S. history. New York made its DTC authorization permanent in August 2024. At least eight additional states introduced bills in 2024–2025, including Texas, Colorado, Pennsylvania, and Maine. If all pending states passed, DTC coverage could reach 40–50% of the U.S. population.

Wine took 20 years after the 2005 Granholm v. Heald decision to go from a handful of states to 48. Spirits won’t take that long—the regulatory infrastructure, compliance technology, and political precedent already exist.

The Demand Is Documented

The 2025 Sovos ShipCompliant/ACSA report surveyed over 2,000 adults:

Source: 2025 DTC Spirits Shipping Report (Sovos ShipCompliant / ACSA / Harris Poll; n=2,004 adults 21+)

The 92% retail synergy figure is the most important number in this analysis. Nearly 20 years of wine DTC data confirm the same pattern: direct-to-consumer success drives subsequent wholesale and retail performance. DTC doesn’t weaken the three-tier system. It feeds it. For investors evaluating distribution-dependent brands: the DTC-to-retail flywheel is the clearest growth signal in the category.

The Distribution Power Structure Is Being Challenged

FTC v. Southern Glazer’s

In December 2024, the FTC sued Southern Glazer’s—$26 billion in 2023 revenue, 44-state operations, approximately one in every three bottles sold in the U.S.—under the Robinson-Patman Act. First enforcement action in over two decades. The allegation: Southern Glazer’s charged small independents “drastically higher” prices than large chains for identical products, enabling chains to resell below what independents paid wholesale.

On April 17, 2025, Judge David O. Slaughter denied the motion to dismiss in its entirety. Despite FTC Chairman Ferguson’s prior dissent from the vote to sue, the Trump-era FTC actively defended the case, filing an opposition brief in March 2025. Combined with the FTC’s January 2025 Robinson-Patman suit against PepsiCo, this signals a broader enforcement trend—and the bipartisan staying power of the case removes the “it’ll get dropped with the new administration” argument.

Southern Glazer’s and RNDC together likely control 55–65% of U.S. wholesale wine and spirits distribution. The next largest, Breakthru Beverage Group, operates in only 13 states. The irony: the three-tier system was designed to prevent exactly this kind of consolidation.

The Provi Settlement: Digital Platforms Win Legal Recognition

Provi, a B2B online marketplace, sued Southern Glazer’s and RNDC in 2022, alleging they conspired to boycott Provi’s platform after processing over 120,000 orders through it between 2016 and 2021. A federal judge denied the distributors’ motion to dismiss in May 2024.

Both cases settled in 2025. The critical outcome: Provi’s marketplace is now a permitted form of ordering for the entire Southern Glazer’s portfolio—a complete reversal. RNDC agreed to build a direct integration. As Digital Commerce 360 reported, the settlement “signals a digital turning point.”

These cases establish two precedents simultaneously. First: dominant distributors face legal risk when their pricing practices disadvantage small retailers. Second: digital platforms have a legally protected right to operate as ordering channels within three-tier. For brands considering platform-based distribution, the legal cover is now explicit.

Framework: State Permeability Assessment

Where does your market stand?

Sources: Sovos ShipCompliant; ACSA; LibDib/RNDC announcements; state ABC agencies

Mississippi, Revisited

In July 2025, Mississippi became the 48th state to allow direct wine shipping—the last significant holdout in a 20-year expansion that began with a single Supreme Court case. The wine industry’s trade groups didn’t celebrate with a press release. They barely mentioned it. Because by 2025, wine DTC wasn’t news. It was infrastructure.

Twenty years earlier, that would have been unthinkable. In 2005, when the Granholm v. Heald decision struck down discriminatory shipping laws, the wine wholesale lobby predicted disaster: underage access would spike, state tax revenue would collapse, and the three-tier system would crumble. None of that happened. What happened was that small wineries survived a brutal consolidation cycle because they could sell directly to consumers who valued their products. The three-tier system didn’t crumble. It adapted.

Spirits are standing where wine stood in 2006. Nine states and D.C. California just opened the door. Eight more are considering it. The wholesale lobby is making the same arguments about spirits that it made about wine—and those arguments have the same shelf life.

The interesting question isn’t whether spirits DTC will expand. That trajectory is as clear as wine’s was after Granholm. The interesting question is what happens to the brands that wait for the system to change rather than building capability now. In wine, the answer was straightforward: the ones that built DTC infrastructure early captured 70% of revenue through direct channels and weathered the consolidation. The ones that waited for their distributors to prioritize them are disproportionately the ones that closed.

The three-tier system isn’t the Berlin Wall. It never was. It’s a set of rules that evolve—and the brands that learn the rules as they actually exist, rather than as they’re assumed to exist, are the ones writing the next chapter.

What’s your experience with three-tier permeability? We’d love to hear from brands, retailers, and investors navigating this landscape.